Johan Castberg comes online, reshaping North Sea supply

Executive Summary

Market & Trading calls

Americas:

- Bullish WCS Hardisty due to the lack of tariffs on Canadian oil, PADD 2 maintenance winds down and Canadian upgrader outages tighten May supply.

- Bearish Castilla and Oriente on rising LatAm exports and reduced USGC demand amid North American tariff exemptions.

- Slightly bullish WTI-Brent spread, as US production faces downside risks with prices around $65/bbl and Brent oversupply looms.

Europe and Africa:

- Bearish on medium crude differentials, with a longer-than-typical European crude and condensate balance over H2 (partly of the back of a ramp up of Johan Castberg) and a faster-than-expected unwinding of OPEC+ cuts expected to keep regional supplies elevated.

- Bullish on Norwegian crude supply, with Equinor commencing oil production from the Johan Castberg field as of 31 March, with 12 of 30 wells now operational.

- Bullish of Ekofisk crude differentials amid planned maintenance during the summer months, which should see a decline in output of the grade.

Middle East - Asia - Russia:

- Stable on freight rates in the Red Sea, which should continue to trend at elevated levels due to continued Houthi attacks and the need to reroute ships via the Cape of Good Hope

- Neutral on Kurdish crude exports as we do not expect a resumption of the Iraq-Turkey pipeline in the near future

- Bullish on OPEC+ output volumes in May since the group decided on larger-than-expected oil supply increases next month, adding 411 kbd rather than 138 kbd

Americas: Canadian, Mexican grades to outperform other Latam heavy sours

Canadian and Mexican crudes are emerging as the clear winners from the US administration’s “Liberation Day” tariff policy shift, which excluded North American barrels. This exemption has amplified a rally in Canadian heavy grades that had already begun on speculation of potential sanctions. WCS Hardisty’s discount to WTI Houston narrowed to under $10/bbl for the first time since Nov., supported by a record 4.42 Mbd of US imports from Canada last week, up 440 kbd w/w, per EIA.

The resilience is likely to persist. TMX arrivals into PADD 5 reached a three-month high of 154 kbd, despite peak West Coast maintenance cutting 470 kbd of refining capacity. Canadian diffs are set for further strength in May as Midwest refinery outages ease and capacity returns—offline units are projected to fall from nearly 600 kbd in April to just 100 kbd. Concurrently, upgrader maintenance in Alberta will cut Canadian output from 5.1 Mbd in Mar. to 4.75 Mbd by May.

Canada oil output, kbd

Source: Kpler

In Latin America, recent strength in heavy sours such as Colombia’s Castilla and Ecuador’s Napo and Oriente appears unsustainable. Castilla briefly traded at a slight premium to WTI, while Oriente and Napo narrowed to -$4.77/bbl and -$7.87/bbl, respectively. These gains were supported by limited supply growth and weather-related disruptions.

However, the absence of tariffs on Canadian and Mexican barrels undermines competitiveness for Colombian and Ecuadorian grades, which are less integrated with the PADD 2 and PADD 3 refining systems. Rising export flows exacerbate the pressure—Ecuadorian shipments rose by 14 kbd m/m to 368 kbd in March despite a SOTE pipeline rupture, while Colombian exports jumped 94 kbd m/m to 508 kbd, with most of the increase (+57 kbd m/m) targeting the US Gulf Coast.

Latam heavy sour grades differentials against WTI, $/bbl

Source: Argus Media

In the US, falling prices now pose a downside risk to our base case for production growth. While we still forecast a 275 kbd y/y increase in 2025 output, WTI hovering near $65/bbl—a level last seen in early December—may force activity to decelerate. Production already slipped to 13.15 Mbd in January, down 270 kbd from Q4 levels, due to severe weather in the Bakken and Texas.

If macroeconomic headwinds persist and capital discipline holds, a forecasted new record of 13.6 Mbd by June is no longer assured. Lower output would narrow the WTI–Brent spread, particularly as Brent faces its own supply overhang from the 220 kbd Johan Castberg startup and OPEC+ hikes in May.

WTI Houston – ICE Brent spread, $/bbl

Source: Argus Media

Atlantic Basin: OPEC+ unwinding comes as a clear boon to European refiners

Crude prices fell sharply on 3 April amid a broader drop in equity markets, with Donald Trump announcing tariffs targeting multiple trading partners, stoking concerns over global trade flows and macroeconomic growth. Additional downward pressure has come from OPEC+, who surprised markets by accelerating the unwinding of their 2.2 Mbd voluntary cuts. which pushed Brent down some $5/bbl, with the European benchmark settling around $70/bbl at the time of writing, representing the bottom of the 12-month range.

The faster unwinding of OPEC+ voluntary cuts comes as a clear boon to European refiners, who rely heavily on crude from the Middle East. Higher availability of crude, coupled with the prospect of weaker global crude demand (amid uncertainty regarding the impact of US tariffs), will keep a lid on crude prices for the time being, particularly for medium-density grades. Additional downward pressure for medium-density crudes will come amid a ramp-up at Norway’s Johan Castberg field (discussed in the section below), adding further length to regional balances, with the European crude balance expected to remain less tight than in previous years over H2.

European crude and condensate balance, Mbd

Source: Kpler

Equinor has commenced oil production from the Johan Castberg field as of 31 March, with 12 of 30 wells now operational, according to the operator. Output is set to reach a plateau of 220 kbd in Q2, which will support regional crude availability over the coming months. Two April cargoes are currently scheduled, with the first sold to Spain’s Repsol. The May loading program features six cargoes of 700,000 bbl each, equivalent to 135 kbd, signaling a steady ramp-up in export volumes. The field’s crude is middle distillate-rich, with an API gravity of 34.7° and Sulphur content of 0.16%. The gradual ramp-up at the field will help offset a rise in natural declines at other developments, lifting Norway’s crude supply above year-ago levels over H2. Robust natural declines and delays to the Johan Castberg project have kept a lid on Norway’s crude output over the first few months of the year, with production remaining around 50 kbd below year-ago levels (see chart below).

Norway's crude and condensate supply, kbd

Source: NPD

ConocoPhillips will conduct a four-week maintenance shutdown in June across the Ekofisk area and the Nordpipe system. While the company has not disclosed the expected export reduction, the Ekofisk and Eldfisk fields—operated by ConocoPhillips—produced a combined 99,000 b/d on average last year, accounting for nearly half of total Ekofisk blend loadings. The tri-annual maintenance could materially tighten the supply of the Ekofisk grade, which underpins the North Sea Dated benchmark and often helps set its price. With inventories already low and seasonal maintenance underway across the region, the expected dip in output may exert upward pressure on Dated pricing during the summer demand window. Although concerns over the broader economic impact of US tariffs could weigh on BFOET crude differentials in the near term, Ekofisk may find support from the anticipated drop in supply.

BFOET crude differentials, $/bbl

Source: Argus Media

Middle East and Asia: OPEC+ decides on larger-than-expected supply increase for May

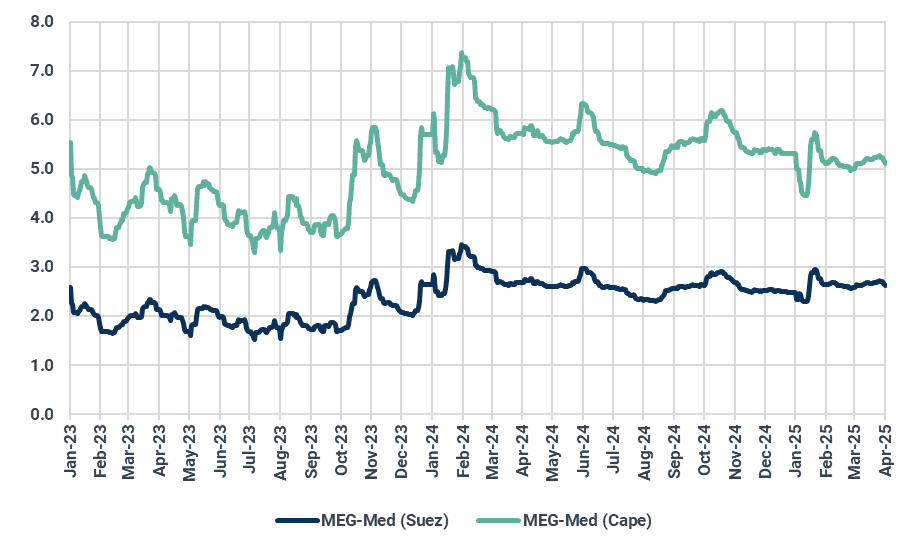

Iraqi crude exports have averaged close to 3.4 Mbd so far in 2025, broadly in line with 2024 levels. Of this, approximately 2.0–2.1 Mbd comprised Basrah Heavy, while 1.2–1.3 Mbd was Basrah Medium. The onset of Houthi attacks in the Red Sea in November 2023 prompted a significant rerouting of Iraqi crude flows. Whereas 100% of Iraq-to-Europe shipments transited the Suez Canal in 2023, that share dropped to just 20% in 2024, with 80% diverted via the Cape of Good Hope. This longer route more than doubled transit times and significantly raised freight costs. In Q1 2025, the MEG–Med Suezmax rate via the Cape of Good Hope averaged $5.2/bbl—nearly $2/bbl higher than the Suez route (see chart). Despite the detour, European purchases of Basrah crude fell only slightly in 2024, averaging 690 kbd, down 30 kbd year-on-year. Following a ceasefire between Israel and Hamas in January 2025, Houthi rebels announced a partial halt to maritime attacks, targeting only vessels with direct Israeli ties. This led to a brief decline in hostilities in the Red Sea, but transit through the Suez Canal remained limited due to ongoing security concerns. By March 2025, tensions escalated once again as fighting between Israel and Hamas resumed, ending the ceasefire. The U.S. responded with intensified airstrikes on Houthi positions, citing renewed threats to commercial shipping. The continued reliance on longer routes around southern Africa is driving up freight rates, eroding the competitiveness of Middle Eastern grades—particularly Iraqi crude—in Northwest Europe and the Mediterranean. Although Basrah Medium is priced lower than Aramco’s Arab Medium on a formula basis, the additional $2/bbl in freight costs from Cape of Good Hope rerouting brings its effective landed price in the Mediterranean to parity with Aramco’s crude.

MEG-Med Suezmax freight rates, $/bbl

Source: Baltic Exchange

In early March, Iraqi Oil Minister Hayan Abdulghani announced that Iraq is considering the option of exporting Basrah crude grades via the Turkish port of Ceyhan, once the Iraq-Turkey Pipeline is reopened—a move aimed at bypassing the expensive route via the Cape. Basrah crude is traditionally exported from the Al Basrah Oil Terminal in the Persian Gulf, with the bulk of volumes shipped to Asian markets, particularly China and India. Before the Iraq-Turkey pipeline was suspended in April 2023—due to a dispute over the Kurdistan Regional Government’s (KRG) independent export authority—the pipeline was primarily used to transport Kirkuk Blend Type (KBT) crude from fields in the Kurdistan Region to Ceyhan, averaging around 400 kbd in Q1 2023, with most volumes destined for Europe. Baghdad has since expressed interest in utilizing the same corridor to export Basrah crude, once flows resume. However, we remain doubtful that a near-term restart is likely, despite a brief surge in optimism in late February. On February 23, the KRG announced an agreement with Iraq’s oil ministry to resume exports of Kurdish crude based on available volumes. Still, the anticipated late-February 2025 restart failed to materialize, largely due to unresolved disputes between the federal government and IOCs operating in Kurdistan—particularly over payment terms and contractual frameworks. Further complicating the situation, Turkey has shown little incentive to facilitate a restart, as its $1.5 billion arbitration dispute with Baghdad remains unresolved.

KBT crude exports, kbd

Source: Kpler

On March 3, eight OPEC+ members—Saudi Arabia, Russia, the UAE, Kuwait, Iraq, Algeria, Oman, and Kazakhstan—agreed to gradually unwind 2.2 Mbd of voluntary cuts beginning in April 2025 through September 2026, adding an average of 138 kbd each month. On March 20, several countries, including Iraq, Kazakhstan, and Russia, announced compensation cuts to partially offset the impact of this unwinding. Today, markets were caught off guard as OPEC+ approved a larger-than-expected supply increase for May, raising output by 411 kbd—triple the originally planned monthly increment—further exacerbating the ongoing slump in oil prices triggered by President Donald Trump’s new tariff regime. On April 2, Trump announced sweeping tariffs on U.S. imports, prompting a sharp sell-off in both oil and equity markets. After settling at $74.95/bbl on Wednesday, ICE Brent futures fell to around $70/bbl in early afternoon trading. The OPEC+ accelerated output hike is intended to reinforce compliance and create space for future compensation cuts. The group will reconvene on May 5 to determine production levels for June.

Agreed oil output reversal over 18 months, kbd

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler.

Expert research & analysis driven by proprietary data

Hey, how can we help you today?

Get in touch and see why the most successful traders and shipping experts use Kpler