Geopolitical uncertainty and weak fundamentals to keep LNG and gas prices stable for the week

Executive summary

European TTF front-month price outlook: Steady

Kpler expects the front-month TTF to remain relatively steady in the coming week. After five consecutive days of price increases driven by escalating tensions in the Middle East, we anticipate that geopolitical risks will continue to exert upward pressure on prices as long as the situation remains volatile. However, fundamentals are expected to stay loose enough to counterbalance these risks. The completion of works on Algerian pipelines and additional volumes from Norway—expected as the planned maintenance season nears its end—should help maintain strong underground storage levels.

Asian LNG front-month price outlook: Steady

Asian LNG prices mainly stabilized only increasing by $0.01/MMBtu w/w to $13.09/MMBtu on 2 October. Even with geopolitical tension and attempted attack in the Middle East, Asian prices haven't been impacted as much as spot demand has been weak due to the peak summer cooling season ending along with recovering supply. LNG prices in Asia are expected to stay stable for the week ahead, driven by continued geopolitical uncertainty as well as potential winter restocking activities and supply outages, mainly from the US balancing weak fundamentals in the region.

US Henry Hub front-month price outlook: Steady

Producers continue to cut supply to buoy the market. Power demand continues to decline substantially as the heating season approaches. US LNG facilities see decreased utilization, hurricane season remains a major threat to feedgas demand. Storage balances getting close to the 5-year average.

Daily thermal fuel rolling front-month prices ($/MMBtu)

Source: Kpler calculations based on ICE and NYMEX

Price movement definitions

Steady – front-month prices move in a 20 cents/MMBtu upside/downside range

Bearish – front-month prices decrease by more than 20 cents/MMBtu

Bullish – front-month prices increase by more than 20 cents/MMBtu

Europe: Escalation in the Middle East close to offsetting relative fundamentals bearishness

The European TTF front-month price increased by $0.29/MMBtu over the past week, or 2.3%, to close at $12.53/MMBtu on 2 October. Prices rallied primarily due to renewed tensions in the Middle East, where Israel launched an incursion into southern Lebanon, followed by a retaliatory missile strike from Iran. Despite these developments, fundamentals remained relatively loose, despite production hiccups in the U.S., particularly at Cameron, Sabine Pass, and Cove Point. EU LNG imports totaled 1.10 mt last week, the lowest since December 2021.

Looking ahead, Kpler Insight anticipates the front-month contract to trade within a range, as loose regional fundamentals counterbalance heightened geopolitical risks.

The escalation in the Middle East remains the most important factor in supporting the bulls. Israel is launching a localized ground operation in southern Lebanon while missiles continue to be fired to and from both countries. Iran has retaliated with a missile barrage, and some missiles were also fired into Houthi-controlled Yemen from Israel. The geopolitical premium is, therefore, expected to remain strong at least until next week.

Other bullish factors include unplanned maintenance due to a compressor failure at Norway’s Troll gas field, which has a capacity of 133 mcm/d. This is expected to limit flows by 15.8 mcm/d until 4 October and by 5 mcm on 5 October. Cove Point is also undergoing planned pipeline maintenance until 10 October, with the last cargo exported on 18 September.

Market fundamentals continued to support bearish sentiment, as more flows are seen from Norwegian pipelines as maintenance progresses, with 22 mcm/d of nominations expected for next week. Similarly, Algerian pipeline flows via Transmed and Medgaz are approaching pre-maintenance levels. Weekly Algerian LNG flows are expected to remain strong with 0.3 mt for this week. This additional pipeline supply has helped fuel more net injections into Europe, with underground storage at 94.2% at the time of writing, according to GIE. Furthermore, temperatures in Western Europe are projected to rise above seasonal levels at the beginning of next week, reducing the need for heating. Gas-to-power demand is expected to remain low to stable as renewable availability is forecast to remain robust over the weekend, along with solid hydro generation and French nuclear output.

Daily Algerian pipeline exports to Spain and Italy (bcm/d)

Source: ENTSOG, Kpler

Asia: Geopolitical uncertainty in Middle East continue to weigh on weak fundamentals

Asian LNG front-month prices increased by $0.01/MMBtu to $13.09/MMBtu on 2 October w/w. This was driven by geopolitical events in the Middle East as fundamentals in the region remain slack with spot demand sidelined while supply largely recovered.

For the week ahead, Kpler Insight expects Asian LNG prices will remain stable as geopolitical uncertainty and slightly lower supply from US will be balanced with weak Asian spot demand. Fundamentally, we view weak spot demand in Asia to continue until large Asian buyers start to begin restocking for winter months.

In Japan, the Japan Meteorological Agency (JMA) predicts 70% chance of higher temperatures for 28 September to 25 October in which we view will result in a delay in winter purchases as buyers work to meet demand in the prompt. Although temperature in most of Japan remain above 30 degrees Celsius, power demand gas declined w/w as inventory levels held by major power companies increased from 1.64 mt to 1.99 mt (according to METI data on 29 September). We view Japanese buyers can still meet prompt demand with term contracts and via time swaps and will remain inactive in spot market until focus switches to winter procurement. The JMA predicts normal or higher temperatures across Japan for the three month period from October to December, so buyers haven't been stimulated to rush back into market to procure for the winter yet. In addition, nuclear capacity is expected to rise as Tohoku Electric is on track to restart the Onagawa no.2 nuclear reactor in November as the company began fuel loading. In addition, Shikoku Electric`s Ikata no.3 nucealr reactor has been operating again in late September coming off from maintenance as expected.

Bearish sentiment continues on demand side as Chinese and South Korean buyers remain sidelined for most of the week ahead as both countries have entered Golden Week from 1 to 7 October. In the prompt, Taiwan is currently facing Typhoon Karathan that has affected deliveries to Taichung terminal. Namely two LNG vessels Al Wakruh and LNG Ebisu based on our ship tracking data has been delayed and idling outside the range of the typhoon. There could be some added bullishness from Taiwan for the upcoming winter as Taipower has announced shutting down coal fired power plants for the upcoming winter in effort to clean the air and to prioritize gas fired power plant to meet power demand.

We continue to view South and Southeast Asian buyers to remain sidelined at current prices above $13/MMBtu, however India has been actively procuring cargoes to meet its peak demand for the festive season. But we view that additional marginal LNG demand growth is hard to materialize as power demand is expected to be met with coal fired generation. In Vietnam we note that a recent tender was not awarded as lack of limited interest in the market to supply a smaller cargo.

Outside of Asia, we note a sharp decline in LNG imports in countries such as Egypt, Argentina, Kuwait where typically these seasonal buyers increase LNG imports to meet northern hemisphere summer for Egypt and Kuwait and southern hemisphere winter in the case for Argentina. Imports into these countries declined from peak of 1.7 mt in July to 1.5 mt in August and 1.4 mt in September thus, indicating a end of peak seasonal summer demand as we head deeper into the shoulder months.

Egypt, Kuwait and Argentina monthly LNG imports (mt)

Source: Kpler

US: Inventories normalize despite weak demand

US Henry Hub front-month prices declined by $0.09/MMBtu last week from $2.82/MMBtu on 25 September to $2.91/MMBtu on 2 October.

Price action was relatively tame this week after tighter storage balances had enabled bulls to push prices higher the past few weeks. Weak power demand and LNG exports both weighed on the market this week. The cooling season has ended, so power demand is declining quickly. Over the last 7 days power burns averaged 37.6 bcfd, 3.9 bcfd lower than the prior 7 days. Power demand is still 34% above the lows seen earlier this year, so there is still a long way to go until it bottoms out. However, residential and commercial heating demand will begin picking up the slack as the temperatures drop.

LNG feedgas demand averaged 11.7 bcfd over the last 7 days, with volumes dropping as low as 10.8 bcf on 30 September. The low on 30 September was due to a short outage at Cameron LNG which recovered to normal volumes the next day. However, volumes out of Sabine Pass fell to 3.9 bcfd on 2 October which is about 20% below their capacity. Cove Point has also been offline since 20 September, reducing demand by 0.69 bcfd. Additionally, Hurricane season remains in full swing and is a major risk that can hurt supply, demand or both.

Despite the intensity of Hurricane Helene, it only reduced GOM production by about 20% or 0.4 bcfd, its path was too far east to disrupt LNG export facilities, and most production platforms were also spared. Regardless, production continued to remain low at around 100.0 bcfd as producers continue to hold back supply.

Tighter storage balances have been a major catalyst for recent increases in natural gas prices. Inventories are much closer to normal levels with a 47 bcf increase in inventories for the week ending 20 September bringing volumes within 4.8% of the 5-year average. Kpler Insight expects a 60 bcf injection for the week ending 27 September, much lower than the 5-year average which is 98 bcf.

Daily US power demand (bcfd)

Source: Kpler, EIA

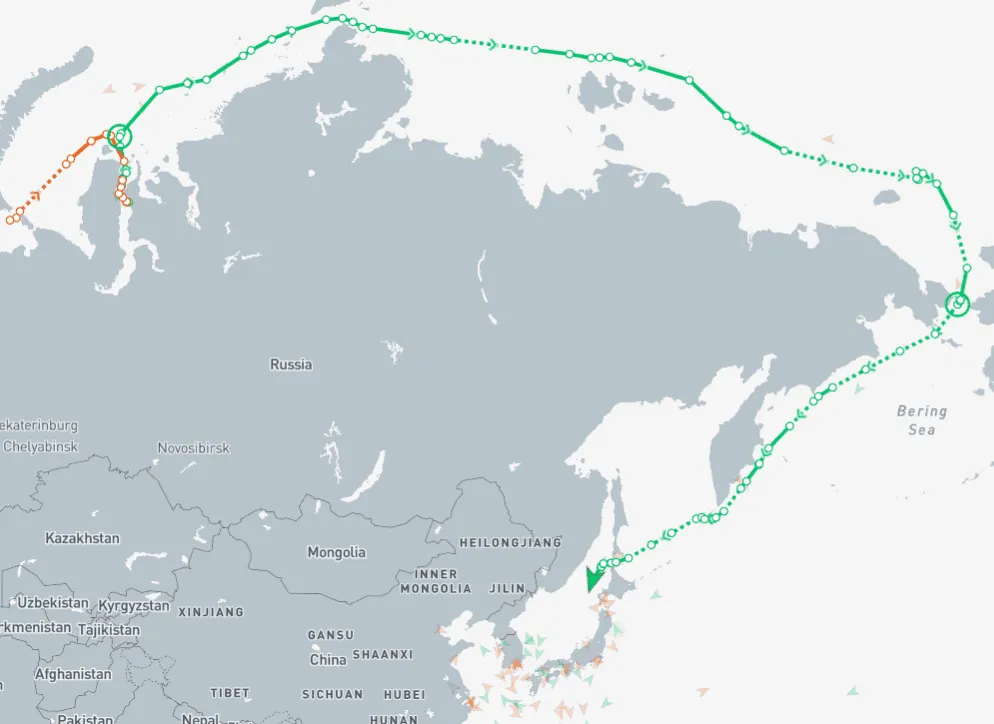

LNG supply: All eyes on Arctic LNG 2 as Asya Energy sails past Kamchatka FSU

Russia’s sanctioned Arctic LNG 2 continues to regularly load cargoes, with the Nova Energy arriving at the facility on 2 October after receiving a suspected cooldown cargo from the Saam FSU in Murmansk around 27 September, according to satellite imagery. We await the final destination of laden vessels on the water – in particular Asya Energy, which has passed the Northern Sea Route, the Kamchatka FSU and the Sakhalin 2 LNG plant, and Pioneer, which has successful passed the Red Sea and is headed east into the Arabian Sea. These cargoes could be destined for end-users in Asia, with Kpler expecting the most likely destination to be China.

Asya Energy current position

Source: Kpler

In the United States, the 5.25 mtpa Cove Point facility remains on planned maintenance after reducing feedgas to zero on 20 September. We expect the works to last 3-4 weeks, in line with the typical timescale. Meanwhile, feedgas deliveries into the 13.5 mtpa Cameron plant saw a one-day slump to 1.12 bcf on 30 September, before recovering to typical levels of over 1.9 bcf on 1 October. The Maran Gas Andros docked outside the facility on 30 September and has yet to leave at time of publication. Elsewhere, feedgas into Elba Island recovered after dropping on 27 September in preparation for Hurricane Francine.

Meanwhile, LNG exports remain weak from Australia’s 8.9 mtpa Ichthys plant. The plant typically loads 2-3 cargoes per week but exports have held steady at one cargo per week since early September as ongoing works to train two impact production. This week, offtakers have reported to Kpler that works at train two could extend into late October.

Kpler Insight offers comprehensive coverage of global LNG, European and US natural gas markets.

- Daily LNG news coverage

- 18-month ahead supply & demand forecasts

- 18-month ahead price forecasts for Asian LNG, TTF and Henry Hub

- Natural gas & LNG weekly report

- Monthly reports: LNG monthly, natural gas monthly, LNG spotlight

Unbiased. Precise. Essential. Curious?

Request access today.

See why the most successful traders and shipping experts use Kpler

Get daily expert-driven research through Insight.