Delays at US LNG projects to raise winter 2024 LNG prices

LNG supply

Kpler Insight is excited to announce that we are showing global LNG supply (historical and forecast) split by liquefaction project. Premium subscribers to the global LNG package can find the breakdown in the “LNG supply by plant” tab in the latest Excel add-on here.

Kpler Insight has slightly decreased our global supply forecast by 0.7 mt for 2024, with total supply now reaching 416.2 mt (+3.3 mt y/y growth). Our supply projections for 2025 increased by 3.7 mt and now projected to reach 435.5 mt (+19.3 mt y/y). LNG exports for September reached 33.3 mt which was a 2% decline compared to August.

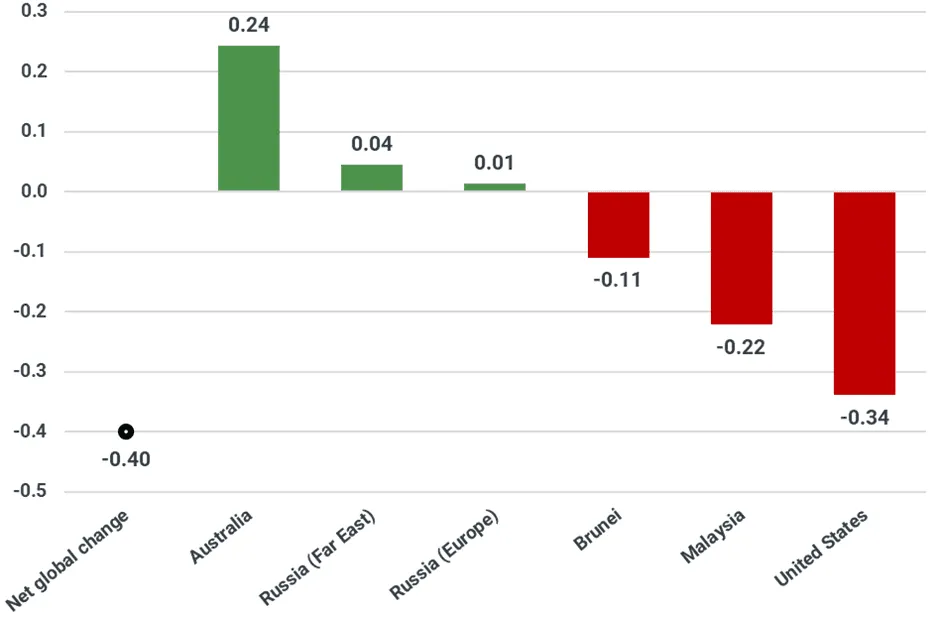

Kpler Insight has also made net downward supply adjustment of 0.4 mt for Q4 2024 and we project supply for the quarter to reach 109.4 mt. These adjustments were largely driven by delays at the Plaquemines and the Freeport debottlenecking projects in the US. Both projects are now slated to start up in January 2025. In addition, minor downside adjustments were made to Bruneian (due to declining natural gas production) and in Malaysian exports (due to lower utilization rates). Upside revisions were made for Australian and Russian LNG exports, as we view natural gas production will remain strong through the winter. Total supply for the quarter was expected to reach 109.4 mt (+1% q/q).

LNG supply change for Q4 2024 compared to Kpler Insight’s September report:

Source: Kpler Insight

For 2025, global LNG supply was slightly reduced to 435.5 mt (0.1 mt reduction compared to our previous report). This was largely due to delaying project start up in the Atlantic Basin. Indeed, Arctic LNG 2 loadings in Russia were reduced to 2.8 mt, and delay expectations in the US (namely Plaquemines and Golden Pass) as well as Qatar (NFE) has pushed some supply into early 2026. This has lowered supply projections for 2025. We have also lowered LNG supply from Brunei, Egypt and Trinidad & Tobago due to feedgas issues. Meanwhile, supply gains were spread across basins, with Algeria leading the way as Kpler Insight has revised upwards utilization rates at the Bethioua and Skikda plants. Australia and the Russian Far East are expected to maintain strong LNG exports throughout the year. In addition, progress towards start up is continuing at LNG Canada, which is still slated to start in January 2025. Train 2 of LNG Canada is now expected to start up in July 2025.

LNG supply change for 2025 compared to Kpler Insight’s September report:

Source: Kpler Insight

LNG demand

Premium subscribers to the global LNG package can find the full 18-month global LNG demand forecast in the “LNG demand by country” tab in the latest Excel add-on here.

Northeast Asian LNG import projections for 2024 increased slightly to 215 mt due to expected higher winter heating demand y/y. We anticipate a historically average winter temperatures compared to a mild temperatures experienced in winter 2023-24. September LNG imports to Northeast Asia reached 19 mt which saw demand grow by 2.5 mt y/y due to prolonged summer temperatures experienced through most of the month increasing the call for gas fired power plants for cooling needs. For 2025 we have increased our demand forecast to Northeast Asia by 3 mt to 217 mt as we anticipate higher gas demand in Japan due to Kpler Insight adjusting nuclear power availability lower based on latest maintenance schedules as well as higher power demand resulting from cooler temperatures projected for 1Q 2025. We have slightly reduced Chinese demand in 2025 as a result of additional pipeline supply above the contracted volumes from Russia to be expected from Power of Siberia pipeline. We continue to anticipate a surplus of LNG supply to enter the second half of 2025, resulting in price-sensitive buyers such as China to increase imports.

LNG demand outlook for South and Southeast Asia in 2024 has been largely unchanged at 62 mt. Minor downward adjustments were made to prompt demand expectations in South Asia as a result of increased coal fired power generation. For 2025, we have largely maintained our view at 67 mt for South and Southeast Asia. We lowered slightly India demand for 2025 reflecting Dabhol import terminal`s historic monsoon season utilization but we continue to view utilization at this terminal to grow in 2025 y/y.

In Europe, LNG imports in September reached 6.4 mt which was 1 mt lower y/y due to ongoing consumption declines (driven by low gas for power demand), weak production growth and strong pipeline deliveries from Norway and Russia. Kpler Insight maintains its view that Russian pipeline gas supply via Ukraine will cease on 1 January 2025, which would lead to the loss of 14 bcm of pipeline supply to the region and support LNG demand in 2025. Although political efforts are underway to potentially substitute Russian gas with Azeri gas, Kpler Insight does not consider it as our base case. LNG deliveries into Europe are projected to increase from 106 mt in 2024 to 116 mt in 2025.

Americas LNG requirements are 0.7 mt higher to 14.1 mt in 2024 and unchanged at 12.8 mt in 2025. The slight increase in 2024 is due to Brazil stepping up LNG intake due to ongoing drought conditions limiting available hydropower and increasing the call for gas fired power. We view Brazil will require less LNG cargoes than the drought of 2021 as renewables now making nearly 35% of current power generation. Our outlook for Argentine LNG imports is relatively unchanged despite improving offtake from the Vaca Muerta shale play. We view Argentina will still likely require LNG imports during the peak winter demand months going forward due to a lack of natural gas storage.

In the Middle East, LNG imports have been revised 0.7 mt higher to reach 11.4 mt in 2024. Higher volumes are expected mostly into Egypt in Q4 2024 due to the full award of Egypt’s 20 cargo buy tender in September. Meanwhile, Kpler Insight has pushed back first LNG imports into Bahrain to summer 2025 as high LNG prices have reportedly delayed purchases. In addition, Bahrain is seeking a sales and purchase agreement (SPA) which is expected to be awarded in Q1 2025. Middle Eastern demand in 2025 has also been adjusted higher by 2.5 mt to 14.6 mt on expectations that Egypt will remain a net LNG importer through the forecast period. We view Egypt will continue to use Jordan`s Aqaba LNG terminal relieving import bottlenecks in 2025.

Region y/y LNG demand change by year (mt)

Source: Kpler Insight

Kpler Insight offers comprehensive coverage of global LNG, European and US natural gas markets.

- Daily LNG news coverage

- 18-month ahead supply & demand forecasts

- 18-month ahead price forecasts for Asian LNG, TTF and Henry Hub

- Natural gas & LNG weekly report

- Monthly reports: LNG monthly, natural gas monthly, LNG spotlight

Unbiased. Precise. Essential. Curious?

Request access today.

See why the most successful traders and shipping experts use Kpler

Get daily expert-driven research through Insight.