US growth concerns rise amid chaotic Trump policy

Market & Trading Calls

- Shifting Market Expectations: While the US economy has shown resilience over the past two years, growing well above trend, markets are increasingly pricing in concerns of a slowdown in growth. 10y bond yields have declined to the lowest levels since early-December, USD has weakened off highs from mid-January, and equity markets are broadly off the highs from earlier this year.

- Policy Uncertainty and Growth Risks: Trump is pursuing a three-pronged economic approach – cut inflation, improve terms of trade, and spread the burden of defense spending among allies. Unfortunately, chaotic, and sometimes inconsistent policy revolving around these three goals is creating uncertainty among businesses and consumers.

- Downside Economic Risks: For now, we will take a middle ground approach around US growth projections. We will revise lower our US growth expectation to 2%, down from 2.5%, albeit we will continue to assume core CPI-based inflation remains stuck in a range between 3 – 3.5%. This inflation assumption is predicated on the fact that immigration restrictions, and tariffs could keep inflation sticky despite lower growth, at least this year.

- Recession Unlikely: Despite policy uncertainty, it is our view that the US economy will avoid a full-blown recession (GDP growth <0%). While chaotic Trump economic policy is disruptive, it is not yet enough to push the US into outright contraction. We see a US recession as less than a 1-in-5 probability at present.

Market Analysis

The market is starting to price in concerns about US GDP growth.

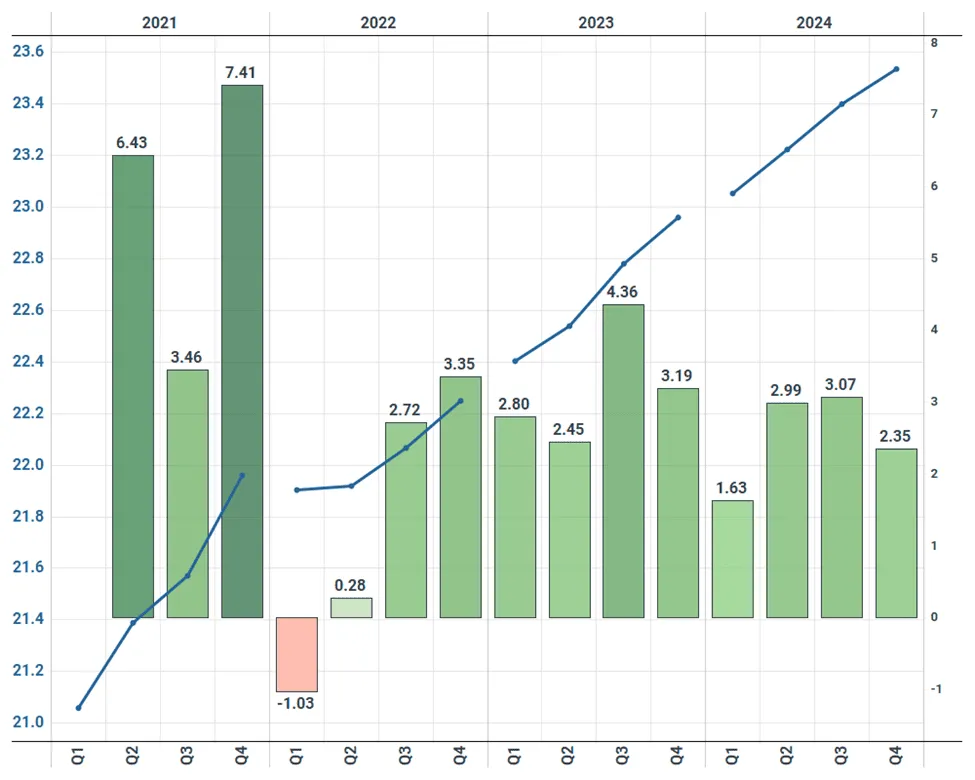

Over the past year, our core argument for the US economy has been one of “no landing” with growth holding at or above trend (2%) alongside an assumption of sticky inflation. This argument was predicated on continued strength across the household consumer, elevated government deficit spending, and a rapid expansion in the labor force. Over the past two years, the US has certainly shown resilience, with GDP growth holding just under 3%, well above long-run trend (2%).

Quarterly US Headline Real GDP (USD tn, left) and Q/Q % Delta Annualized (right)

Source: BEA

Coming into this year, we moderated our growth expectations somewhat. We forecast headline GDP growth of 2.5%, still healthily above trend, but down from a 2.8% rate of expansion in 2024. This was largely meant to account for any increase in uncertainty amid Trump’s return to the White House, and the near certain slowdown in the expansion of the US labor force. We also predicted that core CPI based inflation would hold in a range between 3 – 3.5%, substantially above the Fed’s 2% target. We predicted at most two rate cuts in the second half of the year, with the distinct chance that the committee would pause the cutting cycle altogether. The combination of a strong January inflation print and a healthy employment report bolstered our belief in an above trend growth and sticky inflation narrative.

However, in recent weeks, markets have increasingly begun to price in the possibility of a “growth scare” as chaotic Trump economic policy weighs on both business and consumer sentiment. Long duration bond markets have been the clearest signal. On March 3rd, 10y yields traded as low as 4.16%, marking the lowest level since early-December, and well below a near-term peak of 4.8% seen in January, albeit yields rebounded a bit over the following two days. This yield decline reflects both lower growth and lower inflation expectations for the United States, at least among bond traders. Lower yields might also be a reflection of lowered deficit spending expectations, albeit we remain unconvinced of this argument for now.

Daily US Equity Performance Since Trump Election Victory (%)

Source: FMP

Other key market-based macro variables have also pointed to US growth concerns. Equity markets have cratered with SPX down more than 3% just in the past week after the index failed for a third time this year in mid-February to durably push through a post-election ceiling of 2,100. The Russel 2000 and NAS have both declined by even larger amounts. The DXY Dollar index has also eased, down by more than 4% since mid-January amid narrowing interest rate differentials and expectations of lower US growth. EUR/USD has skyrocketed back towards 1.07 following aggressive new German stimulus measures, meant to bolster defense and public investment.

Consumer sentiment is mixed, albeit one should be careful in reading too much into surveys, which can be highly biased by the political environment. Both the S&P and ISM measures of US services PMI remain in expansion, but have eased off levels seen through the second half of last year. A joint YouGov/Economist poll has also seen the percentage of respondents indicating a worsening economic environment edge up to 43% over the past month, up from 35% in late-January.

Weekly US State of the Economy Poll (%)

Source: YouGov/The Economist

Trump is pursuing policy in a chaotic way that could ultimately push US growth below trend if the administration continues down this path.

The Trump administration ultimately wants to achieve three key economic policy aims – cut the inflation rate, dramatically reduce the current account deficit with the rest of the world by reshoring high value-added manufacturing and improve defense burden sharing among allies who sit under the US security umbrella. The pursuit of these three policies largely utilizes tariffs threats, with the eventual aim of a structurally weaker USD, and lower energy prices.

Unfortunately, the Trump administrations pursuit of lower inflation, improved terms of trade, and defense burden sharing has been chaotic and inconsistent through the first several weeks of his administration, making it difficult for firms and consumers to understand what lies ahead. This uncertainty is made worse by the pursuit of policy that does not necessarily support Trump’s core aims, including restrictions to immigration, and a continuation of heavy amounts of deficit spending, both of which are inherently inflationary. Immigration restrictions also pressure the US labor market, which will need to expand rapidly if the US has any hopes of increasing its manufacturing base.

Quarterly US Current Account Balance (USD mn)

Source: BEA

Even Trumpian tariff policy, which could help to reduce Americas trade imbalances, is being implemented with little forward certainty. If the goal is to incentivize manufacturing reshoring, businesses need certainty that tariffs will remain in place, prompting a higher US price level that would allow domestic manufacturing to profitably operate. Even if the intent is the use of tariffs to force some sort of Mar-a-Lago accord that structurally weakens USD requires policy consistency that is currently not evident.

Many economists, including myself, have been reminded in the post-Covid era of just how resilient the US economy can be. One should always be careful in assuming a recession or sizeable deceleration in growth unless something truly breaks (think financial crisis or a pandemic). Nonetheless, inconsistent and uncertain economic policy out of the White House presents distinct risks for US growth this year.

A month ago, our core assumption was that that the Trump administration would quickly resolve tariff issues with Canada and Mexico, while gradually continuing to increase tariffs on China. Under this assumption, we forecasted US growth at 2.5% this year alongside core CPI-based inflation stuck in a range between 3 – 3.5%. A month later, we still hold to this outcome, albeit with less certainty. Admittedly, the Trump administration looks increasingly determined to move ahead with broad-based tariff implementation on Canada and Mexico, and tariffs on Europe also look likely to move forward, albeit for how long remains anyone’s guess. Even if Trump does end up forging a deal, the month-to-month uncertainty witnessed so far is a net negative for US businesses and consumers.

Monthly US Headline and Manufacturing Industrial Production Index

Source: Fed

As we laid out in our US macro update a month ago, under the scenario of broad-based tariff implementation (i.e., tariffs on all major US trading partners) there are two outcomes. The first is that US inflationary pressures rise amid an increase in import prices, with some offset via stronger USD. Higher prices incentivize manufacturing reshoring, which limits the drag on consumption as reshoring helps to create jobs and support healthy wage growth. Under this scenario, growth remains at or above trend, but core CPI-based inflation is sticky close to 4%.

The second potential outcome under broad based tariff implementation once again assumes inflationary pressures rise at home. However, higher prices fail to incentivize manufacturing reshoring. This in turn exacerbates the drag on household consumption and US economic growth. Under this scenario, we assume real growth falls to a range between 1 – 1.5%, albeit inflation would eventually ease back towards 2% amid weak household consumption, eventually providing the Fed space to cut rates if needed.

We tend to skew towards the second outcome as growing in likelihood this year if broad-based tariffs remain in place for a long period of time, that is, a “low growth” scenario for the US. High amounts of uncertainty paired with aggressive tariff implementation are net negatives for US businesses and consumers. Whether the Fed feels the flexibility to cut more than expected this year will largely depend on inflation. Weaker US growth should weigh on inflation, but immigration restrictions and tariffs themselves could add sticky inflation pressures. We would not bet on an aggressive cutting cycle.

For now, we are taking a middle of the road approach. We will scale back our US growth forecast by 50bp to 2%, in line with long-run trend, still a relatively healthy economic outcome. While market signaling, mixed sentiment, tariff uncertainty, and immigration restrictions give us pause, we need more real data (consumer spending, jobs data, industrial production) to get a better sense of where all of this is heading. However, we will keep to our expectation for sticky core-CPI based inflation in a range between 3 – 3.5%, well above the Fed’s 2% target.

Monthly US Core CPI-Based Core Inflation Over Previous Month and Previous Six Months (%)

Source: Fed

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

.jpg)

.jpg)