Trump weighs Chevron waiver as Ecuador's outages tighten heavy crude markets

Executive Summary

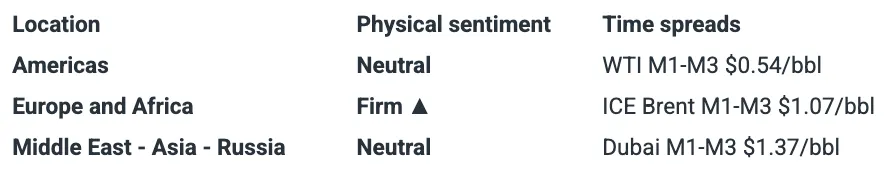

Market & Trading calls:

Americas:

- Bullish on global balances as a potential extension of Chevron's license to operate in Venezuela keeps supplies of heavy sour crude above expectations and elevated over the coming months.

- Bearish on heavy sour crudes across the America's, such as Mexico's Maya, Canada's Cold Lake Blend, and Colombia's Castilla, as a possible extension of Chevron's license keeps competing grades from Venezuela elevated.

- Bearish on Ecuador's crude production as supply outages, due to a temporary shutdown of the country's Sote pipeline in mid-March, keeps a lid on output and flows in March, although output is set to recover fully by late March.

Atlantic Basin:

- Bullish on Turkey's imports of NWE, MED and Latam grades as Tupras fully moves away from Urals.

- Slightly bearish on Kazakhstan's production and exports as CPC exports have remained steady in March.

- Bullish on North Sea crude differentials on lighter-than-usual refinery maintenance in NWE and strong gasoline cracks.

Middle East and Asia:

- Bullish on China’s crude oil demand as both CDUs at the 400 kbd Yulong refinery are set to become operational, while the shuttered 120 kbd Changyi refinery nears a potential restart.

- Bullish on arbitrage crude flows to Asia as the Brent-Dubai EFS has narrowed to near parity, making long-haul cargoes more attractive.

- Bullish on South Korea’s crude purchases as the government pushes to expand stockpiles amid heightened geopolitical tensions.

Americas: Ecuadorian supply outages and a possible extension of Chevron's license disrupt heavy crude markets

The 2025 global crude and condensate balance has narrowed to near parity following recent data revisions (see latest Crude Oil Balance dataset). Stronger crude demand across Saudi Arabia, Europe, Brazil, and China, coupled with lower supply from Mexico and Venezuela, have been the primary drivers of this tightening. A key factor has been Venezuela’s anticipated production decline linked to Chevron’s waiver removal, though recent developments suggest output losses may be more gradual than initially forecast. The Trump administration is reportedly considering an extension of Chevron’s license to operate in Venezuela, while also exploring financial penalties on nations doing business with Caracas, following talks with Chevron’s CEO. Alternatively, PDVSA has announced plans to take over Chevron’s operations, which could mitigate near-term supply disruptions. While uncertainty remains elevated, we continue to expect Venezuelan output to trend lower, with production projected to fall by around 150 kbd from current levels of 900 kbd by year-end, with further downside risk if US sanctions are tightened or extended to other entities trading Venezuelan crude.

Venezuelan crude and condensate supply, Mbd

Source: Kpler

An extension of Chevron’s license would keep Venezuelan crude flows to the US Gulf Coast steady for now, with seaborne shipments to the region accounting for roughly 250 kbd of Venezuela’s exports. However, a potential waiver removal would largely benefit Chinese refiners, who are well-positioned to absorb additional volumes. While Venezuelan exports remained subdued in early March, flows are expected to pick up over the coming weeks, with China reportedly securing around 14 mbbls, or 450 kbd, of heavy sour crude this month. Market sources suggest Chinese purchases will rise further in April, displacing barrels previously bound for the USGC. This sustained demand has kept Venezuelan crude prices firm, with Merey trading at a $5/bbl discount to June Ice Brent—narrower than the $10/bbl discount seen last year. Typically, Venezuelan cargoes take around three months to reach China, involving STS transfers offshore Brazil or Malaysia. Any further tightening of US sanctions could pressure Merey differentials but would likely provide support to competing heavy sour grades in the Americas, including Mexico’s Maya, Colombia’s Castilla, Canada’s Cold Lake Blend, and similar US and Brazilian crudes.

Venezuelan crude exports by destination, kbd

*(March data is preliminary and subject to change)

Source: Kpler

The temporary shutdown of Ecuador’s Sote pipeline has driven a sharp drop in the country’s crude output, further tightening America’s heavy crude markets, already strained by the looming threat of US tariffs on imports from Mexico and Canada and escalating sanctions on Venezuela. A 13 March landslide ruptured the pipeline, spilling approximately 3,800 bbl of crude and prompting Petroecuador to declare force majeure, halt its operations, and shut in production, while several private and international producers also suspended output. Ecuador’s crude production subsequently fell by 35% to 304 kbd on 18 March, down from 468 kbd prior to the incident. While Petroecuador initially considered rescheduling export commitments—including Shell’s recent 1.8 mbbl Oriente tender—repairs were completed ahead of schedule, with the pipeline resuming operations on 20 March. As a significant portion of Ecuador’s seaborne crude supplies US West Coast refiners, any disruption to flows typically lends upward support to competing heavy grades such as WCS Hardisty. In February, Ecuador exported around 90 kbd to the USWC, with roughly two-thirds comprised of medium sour Oriente and the remainder heavy sour Napo.

Ecuador’s crude and condensate supply, kbd

Source: BCE

Atlantic Basin: Tupras shifts away from Urals, turning to European and LatAm grades

Turkey’s Tupras has effectively halted imports of Russian crude, with the last Urals cargo discharged at Aliaga on February 11. The move follows U.S. sanctions imposed on January 10 targeting Russian oil firms and tankers. Tupras was the largest Western buyer of Urals post-Ukraine war, averaging 175 kbd in 2024, or 46% of its total seaborne crude imports.

Since February, the refiner has diversified its crude slate, ramping up purchases of medium sour grades from Aramco and Equinor’s Johan Sverdrup, alongside new imports of medium sweet Guyanese crude (Payara Gold, Unity Gold). Guyanese crude arrivals have averaged 105 kbd so far in March—up from just 8 kbd in 2024. Additionally, Tupras has increased intake of light sweet grades such as Forcados and Libya’s Es Sider, with three Es Sider cargoes totaling 92 kbd MTD.

This shift has supported regional differentials, with Es Sider’s spread to NSD flipping from a -$0.40/bbl discount last week to a +$0.45/bbl premium, despite strong Libyan exports.

Tupras oil imports by grades, kbd

Source : Kpler

Recent attacks on CPC infrastructure have raised concerns over supply disruptions, but Kazakhstan’s exports and inventory levels suggest limited impact. The February 17 drone strike reportedly hit the Kropotkinskaya oil pumping station—the largest in the CPC system—while another attack on March 19 was denied by the CPC consortium.

Despite these incidents, CPC loadings from Yuzhnaya Ozereevka fell only slightly by 52 kbd to 1.6 Mbd in March, staying just below the 1.7 Mbd loading target. With Kazakhstan submitting a new compensation plan to OPEC+ following higher-than-allowed February production (driven by strong Tengiz output), April CPC allocations remain unchanged at 1.7 Mbd, pointing to a limited output decrease. We estimate a 57 kbd drop in Kazakh crude output in April m/m, driven by OPEC+ pressure rather than physical constraints.

Differentials for CPC blend gained $0.37/bbl w/w, now assessed at -$6.56/bbl vs NSD. A narrow Brent-Dubai EFS spread has incentivised Asian demand, with 31% (466 kbd) of CPC shipments since February headed to China and South Korea, supported by strong gasoline cracks in Asia.

MED light sweet grades differentials against NSD, $/bbl

Source: Argus Media

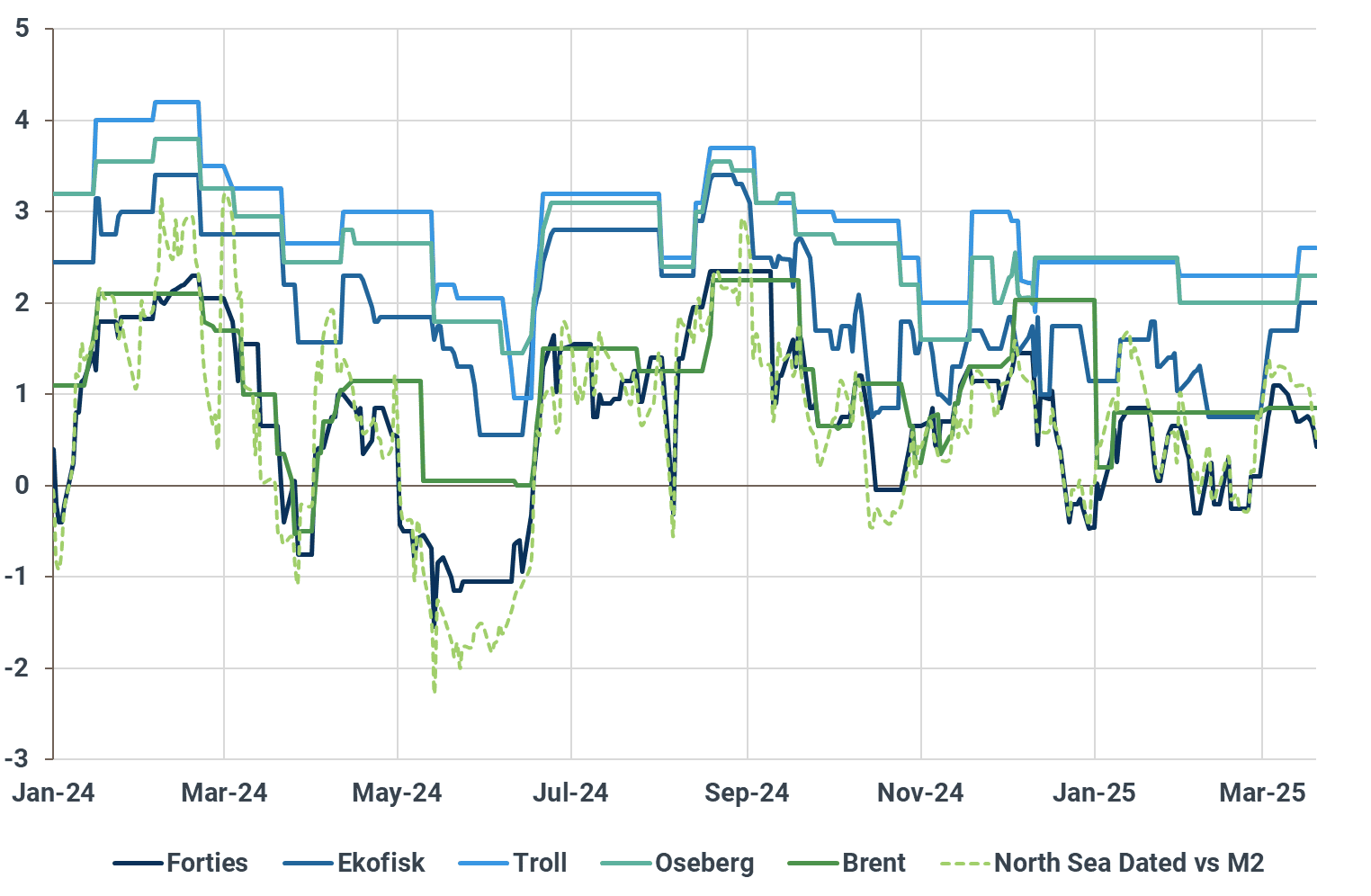

The light NWE refinery maintenance schedule continues to support North Sea crude differentials. Offline refining capacity in the region will average just 460 kbd between March and May—far below the 935 kbd recorded last year. This has buoyed differentials for light sweet North Sea grades, with Oseberg, Ekofisk, and Troll all strengthening by $0.30/bbl w/w, while light sour Forties weakened by $0.20/bbl w/w. Medium sour Johan Sverdrup remains flat w/w at a premium of $1.15/bbl, supported by steady intake from Porvoo (Neste) and Gdansk (PKN Orlen), both of which will remain fully operational through spring.

Additionally, gasoline cracks have outperformed other product cracks in NWE, adding further support to BFOET differentials. This trend is expected to persist as Dangote’s RFCC unit faces operational issues, with a potential shutdown expected between May and June. This comes ahead of peak summer gasoline demand, further boosting demand for North Sea light sweet grades in NWE gasoline-focused refineries.

BFOET differentials against NSD, $/bbl

Source: Argus Media

Middle East and Asia: China’s 400 kbd Yulong ramps up crude buying ahead of new CDU startup

China’s mega-sized Yulong refinery is set to bring its No.1 200 kbd CDU online later this week, according to market insiders. Situated on an artificial reclamation island in Shandong province, Yulong commissioned its No.2 200 kbd CDU in September 2024 and is believed to have been running it at near full capacity. Despite being designed to process medium sour crude like Saudi and Kuwaiti grades, the refinery has yet to commit to any term contracts. This month, Yulong has bought at least 2 Mbbls of Oman crude and 1 Mbbls each of Mostarda, Dalia and Pazflor for May arrivals, along with some ESPO cargoes. The launch of the new CDU is expected to put further pressure on refining margins in China, where refiners are already grappling with a surplus of refined products and weakening fuel demand amid the energy transition and sluggish economic growth. While Yulong is believed to have struggled to stay in the black, the upcoming peak maintenance season could provide an opportunity for the refinery to boost sales and revenue. Some 1.38 Mbd of refining capacity is set to go offline for maintenance in April, followed by 2.03 Mbd in May.

Meanwhile, Shandong-based private refiner Hongrun Petrochemical has acquired Sinochem’s 120 kbd Changyi refinery, likely for 3 bn RMB. Changyi has been shuttered since May 2024 and later went bankrupt due to poor margins and a prior tax evasion case. Some market participants expect Changyi to restart operations as early as May, but this would require Hongrun to secure a crude import quota for the refinery. The timing of Changyi’s reopening is challenging, as a wave of new refining capacity—including the aforementioned Yulong refinery—is set to come online, while China’s new fuel oil tax rebate policy is significantly squeezing teapots’ earnings.

China’s refinery operation rate, %

Source: SCI

The May Brent-Dubai EFS traded in rare negative territory at -$0.18 on Thursday, a situation last seen in November 2023. This comes as the Dubai market remained firm, supported by resilient demand for medium sour grades—though significantly weaker than in the past two months—while sentiment in the Brent market turned even more bearish after Russia and Ukraine agreed to a 30-day halt on strikes against each other’s energy facilities. Average Brent-Dubai EFS was $0.43/bbl so far in March, compared to $0.64/bbl in February and $1.5/bbl in January. The narrowing Brent-Dubai spread has prompted Asian refiners to increase purchases from more distant regions, including Brazil, West Africa, Canada and Kazakhstan. Argus Media reported that Chinese refiners have snapped up nearly 20 mb of Brazilian crude for June arrival, an increase of 2.8 mb from May levels. Kpler data showed that China’s imports of Brazilian oil rose by 5.7 mb month-on-month to 22.25 mb in February. March arrivals are expected to decline sharply as Middle Eastern grades were assessed to be cheaper than Brazilian cargoes, but April imports are set for a strong rebound amid improving competitiveness.

Brent-Dubai EFS, $/bbl

Source: Argus Media

South Korea plans to expand its domestic crude oil reserves beyond 100 mb in 2025 by adding approximately 500 kb to its strategic stockpiles, media reported earlier this week. Kpler data shows that the country currently holds around 95.88 mb of onshore crude inventories, including 56 mb in strategic reserves. The target comes as the world’s fourth-largest crude oil importer commits to strengthening energy security in preparation for potential supply tightness amid ongoing geopolitical uncertainties. South Korea imported 2.8 mbd of crude oil in 2024, steady from a year ago, with approximately 72% sourced from the Middle East. Recently, the country has increased its purchases of Kazakhstan-origin CPC Blend and US crude amid a relatively weaker Brent and WTI compared to Dubai.

South Korea’s onshore crude oil inventory, mb

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

.png)