Refined Products Weekly

Market & Trading Calls

Light Ends:

- Tightening US balances amid refinery maintenance and potential weather-related supply disruptions should buoy West of Suez cracks w/w until H2 January

- However, flexi-crackers switching to propane, softening blending demand in Europe will ensure cracks only modestly rise w/w

- Tightening Russian, Chinese balances, and ongoing Middle Eastern refinery maintenance will put a floor under otherwise weakening fundamentals as flexi-crackers temporarily switch back to propane and while crackers ex-China keep operating rates muted this month

- As such, Asian naphtha cracks will be largely flat over the next couple of weeks

Gasoline:

- Neutral-to-bearish on West of Suez cracks as high stocks will take time to reduce amid sluggish January demand and maintenance in the USGC is unlikely to provide a significant boost.

- Neutral on Singapore cracks as higher exports from China will counteract some of the increased buying due to select outages.

Middle Distillates:

- Still narrow E/W but WoS pull is growing: USGC refinery turnarounds will eventually require NWE to source cargoes from the East.

- Brazil’s currency woes cannot be ignored for long: Brazilian imports may struggle to recover as VAT changes and a weak real could constrain flows.

- Persistently tight EoS: China’s VAT changes continue to keep Singapore spot premiums elevated.

Residue:

- Asian HSFO Cracks: Benchmark Asian cracks face downward pressure from slowing policy-induced China import demand, however, looming Lunar New Year holidays could dampen near term imports. In the longer term, tighter US sanctions enforcement against Iranian oil exports could limit the downside to Asian HSFO cracks.

- US HSFO cracks: Bearish near term due to rising offline capacity but could stabilize as imports and inventories tighten further.

- Europe: Neutral to bullish as constrained imports and Middle Eastern maintenance sustain support for HSFO margins. Meanwhile, limited arbitrage opportunities to Asia weighs on regional VLSFO cracks.

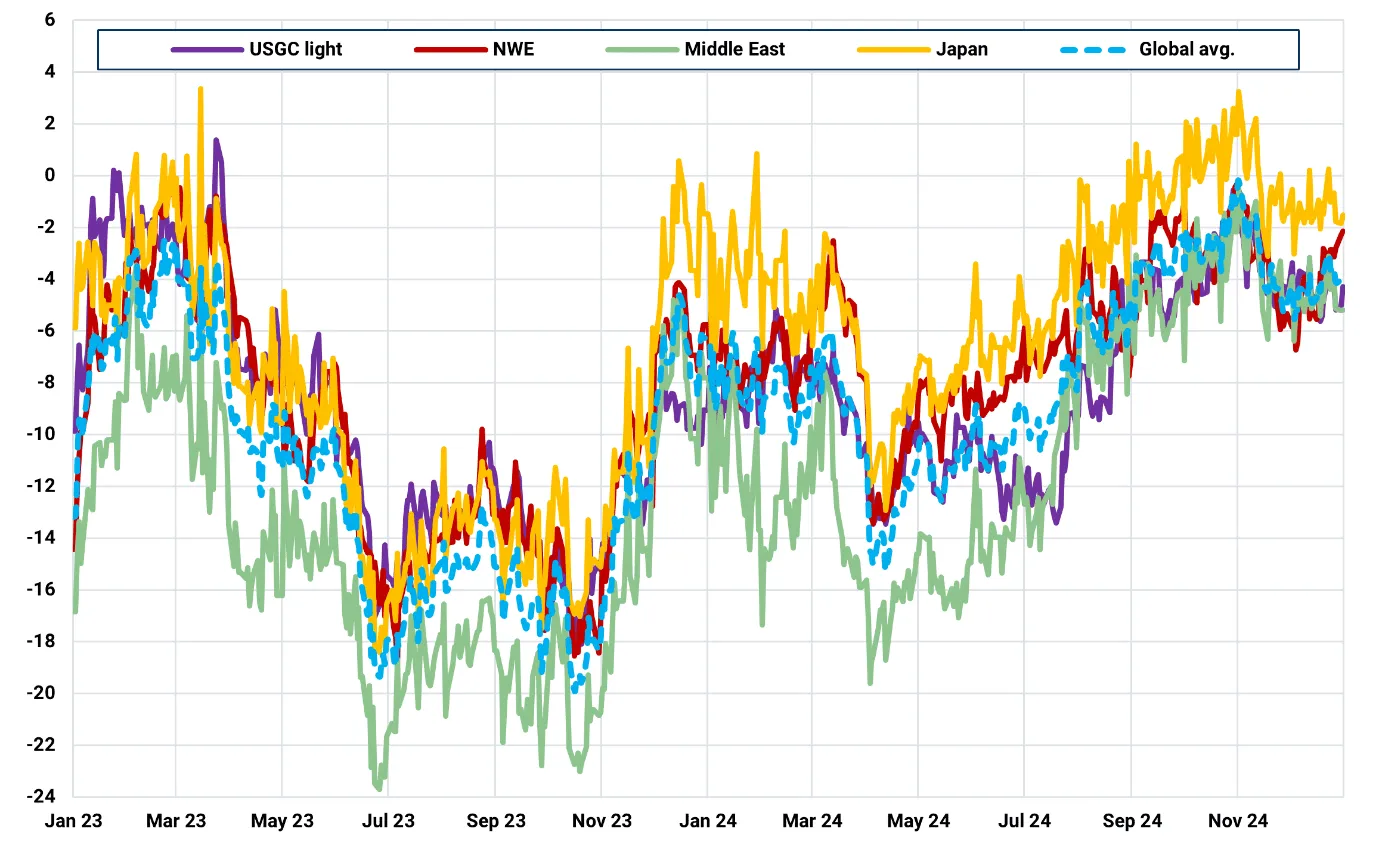

Light Ends: Naphtha cracks inch lower as propane cracking returns

Light naphtha cracks ($/bbl)

Source: Kpler calculations using Argus Media prices

Global naphtha cracks edged lower w/w, as softening fundamentals in the benchmark Japanese market pulled East of Suez values down despite a modest recovery in European cracks.

West of Suez

Fundamentals are set to tighten from next week as refinery maintenance picks up. IIR data forecasts US primary distillation turnarounds will surge m/m to 1.18 Mbd in January, which will weigh on exports. Despite high refinery runs and natural gasoline output in the US over Q4, exports have barely grown y/y following a specification change in October allowing for a higher blend of light ends into winter gasoline.

Meanwhile, there is upside risk to US refinery outages amid weather forecasts predicting a cold snap over much of the US over H1 January which could lead to unplanned maintenance, as has occurred in past years.

That said, West of Suez balances should not tighten too much over the next couple of weeks with demand looking weaker than anticipated last month.

In West Africa, the partial restart of NNPC’s Warri refinery (125 kbd) this week will add to the concern around naphtha blending demand in Europe as refiners reliant on gasoline exports to Africa will continue to struggle.

More significantly, gross naphtha cracking margins have turned negative for the first time since early November 2024 and have fallen to their lowest level versus propane since last July. The unseasonal favorability of propane will put a dent in naphtha cracking demand this month, ensuring naphtha cracks do not rise much versus the five-year average. However, we expect naphtha to become favored again from H2 January as propane fundamentals tighten over the coming weeks.

NWE gross complex steam cracking margins per ton of ethylene ($/t)

Source: Kpler calculations using Argus Media prices

Looking ahead, the prospect of falling US exports this month means the tug of war between NWE and Asia for Med swing barrels will see a few more cargoes clear West than originally anticipated. However, dire European blending and cracking demand will put a firm lid on how many barrels are needed until flexi-crackers switch back to naphtha toward the end of the month.

Med naphtha arbs ($/t)

Source: Kpler calculations using Argus Media prices

East of Suez

In the Middle East, ongoing refinery maintenance through to mid-February will continue to cap exports, which were virtually flat y/y in December. Meanwhile, Russia’s balance is looking tighter than we expected last month following news that Sibur’s 600 kt/year naphtha-fed cracker in Nizhnekamsk began ramping up in late-December.

At full rates, which will likely be achieved by end-February, the cracker will process 47 kbd of light naphtha. The increased cracking demand will therefore largely offset rising supplies from Novatek’s third condensate splitter in Ust-Luga which reached full rates in Q4 and can yield circa 60 kbd of naphtha. As such, despite falling refinery maintenance, Russia’s naphtha exports will only moderately grow on a y/y basis this month.

In relation to demand, fundamentals look bleaker over the next couple of weeks with propane cracking more favourable on a net basis, encouraging flexi-crackers to switch back to the lighter feed. In Northeast Asia (NEA), naphtha cracking economics versus propane are at their weakest since April 2024. However, much like in Europe, we expect this unseasonal switch to be temporary with Chinese PDH margins improving and the prospect of a cold snap in the US buoying propane prices, making naphtha more favourable again from H2 January.

NEA gross naphtha vs propane cracking margins ($/t)

Source: Kpler calculations using Argus Media prices

Beyond January, the outlook remains clouded by the prospect of rising tariffs or a full-blown US-China trade war weighing on fundamentals versus China’s new stimulus package announced last month geared towards consumption. For the time being, new crackers ramping up in China and Indonesia this quarter will put a floor under otherwise weak cracking demand as crackers ex-China will be forced to keep runs historically low to avoid a deepening glut in the base chemical market.

Global naphtha cracks ($/bbl)

Source: Kpler calculations using Argus Media prices

Gasoline: East/West divergence becomes less pronounced as cracks converge

Gasoline cracks ($/bbl)

Source: Kpler, using pricing data from Argus Media

West of Suez

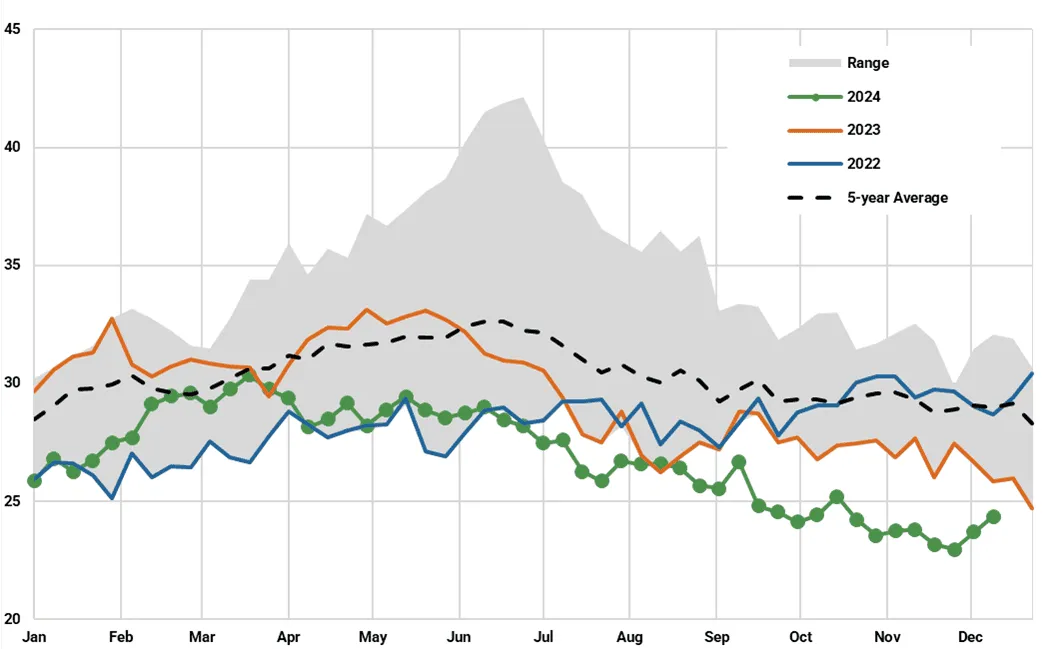

Differences between regional cracks have become less pronounced as declining values in PADD 1 and Asia met a broadly stable and weak European market. Indeed, European gasoline cracks have few short-term prospects to improve. European and Mediterranean refineries will have added substantially to stocks during December, not just in ARA as is evident in the second chart below, but inland too. Given expected balances for January, where demand should seasonally dip, a sluggish start to the year should be expected. This overhang will take some time to deal with especially as the export situation will provide no easy answers.

ARA: gasoline stocks in independent storages (Mbbls)

Source: Kpler calculations based on Global Insights data

Indeed, for European exporters there remains little to be cheerful about. Volume to PADD 1 is the lowest for December since 2018 and the flow to West Africa for the same month is the lowest since 2016, down 182 kbd y/y. News that NNPC’s Warri refinery has returned to limited operations after multiple years of being out of action should not trouble the gasoline market, as any production beyond straight-run products would so far seem to be unlikely.

The wider Atlantic basin will likely lengthen as maintenance in the USGC is lighter y/y although the continued slow and uncertain commissioning of the Dos Bocas refinery is sustaining imports. There could be a bump in interest to cover February maintenance at the Bayway refinery, but the USGC via pipeline and East Coast Canada through cargoes would seem to be best positioned to fill those gaps as it has been the case recently, rather than Europe.

East of Suez

The Singapore crack fell sharply over the end of the year, reaching the lowest level since early October, after shedding nearly $2.50/bbl since mid-December despite an RFCC outage in South Korea driving some strength. There are reasons to be cautious about a substantial improvement in cracks as the incentive to export out of China has increased despite being low for much of December due to tax revisions. Consequently, while the export program was heard to be in the region of 700kt in January, more volume could end up being exported than initially reported. Refinery outages in the region are barely changed m/m but with Pertamina’s Cilacap refinery undergoing maintenance on its larger CDU this month and into early February, some of the increase in cargoes can likely be absorbed by the overall market.

China-Singapore gasoline arbitrage ($/bbl)

Source: Argus Media

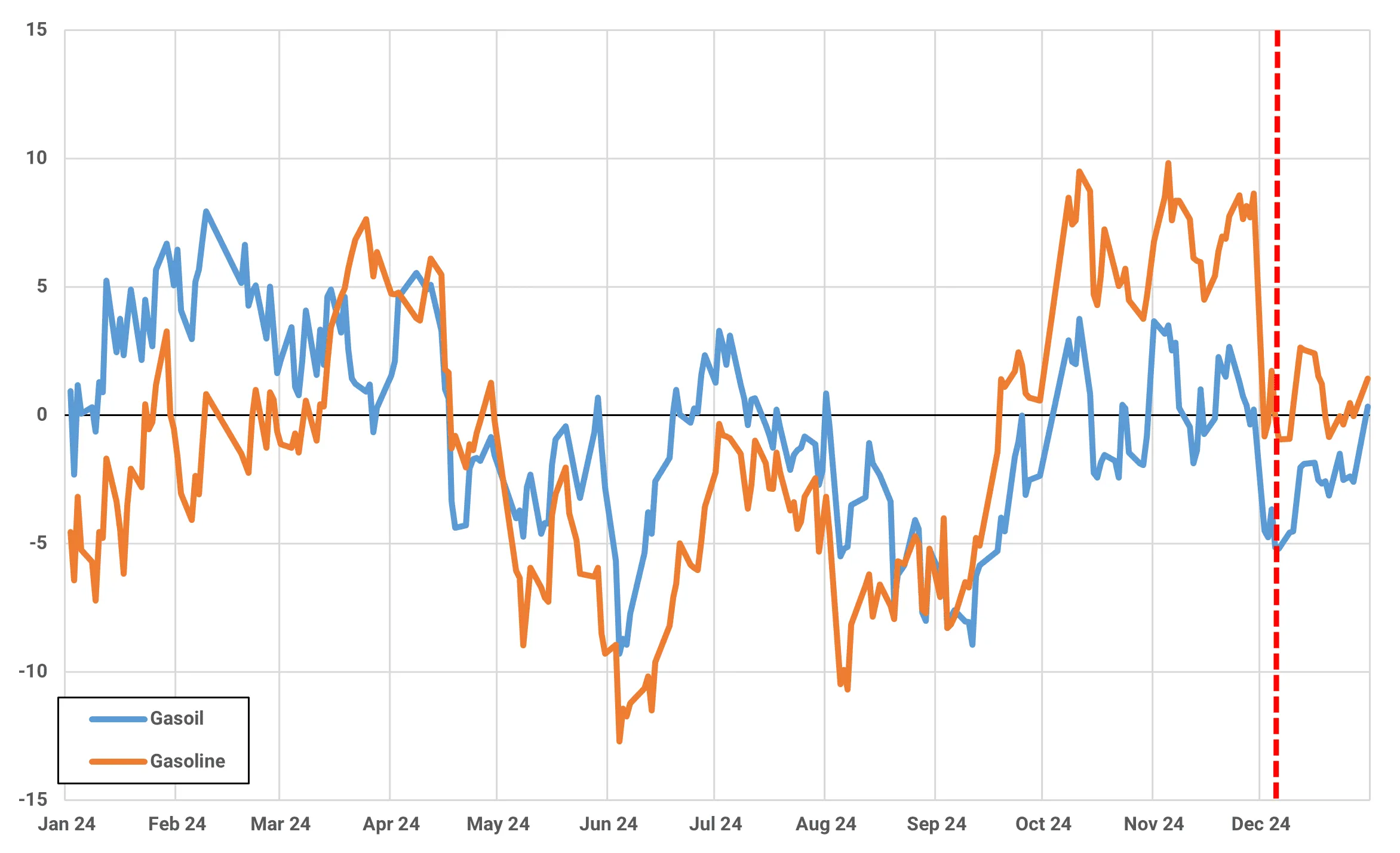

Middle Distillates: USGC maintenance will support prompt cracks

West of Suez

The NWE gasoil market has gained support from several factors, including imports hitting a multi-year low last month, a significant 2.2 Mbbl drop in ARA stocks since November, ongoing refinery issues, and German tax increases driving heating oil purchases during a cold snap across the continent.

ARA: gasoil/diesel stocks in independent storages (Mbbls)

Source: Kpler using Insights Global data

This momentum is expected to persist as the continent’s reliance on USGC cargoes amid a narrow East/West spread faces disruption. PADD 3 refinery maintenance will peak at 1.12 Mbd this month, necessitating higher NWE cracks to attract cargoes from Middle Eastern and Indian refiners.

The E/W spread will need to widen further for East-West gasoil flows to recover from their current multi-month lows. This trend could intensify as Brazilian demand rebounds deeper into Q1. However, the recent recovery of Russian exports to a five-month high in December may limit any substantial tightening of the WoS market.

Gasoil East/West swaps ($/t)

Source: Argus Media Pricing

Additionally, the depreciation of Brazil’s real against the dollar and the upcoming VAT hike in February lower the likelihood of a tighter WoS market later in Q1. If the real continues to weaken, Brazil may eventually resort to government-to-government deals to secure future diesel supplies.

East of Suez

The East of Suez market appears relatively weaker, with balances showing a surplus of 1.13 Mbd. However, China accounts for 625 kbd of this surplus, and recent tax regime changes have severely undermined their export incentives.

China-Singapore arbitrage incentive ($/bbl)

*Values after red line reflect new 4% VAT

Source: Argus Media Pricing

Some view the government’s move to allocate more quota volumes under the tax-free “processing trade” route as an olive branch to refiners. While this narrative is appealing, leviable exports still account for over 80% of total quota volumes, and smaller refiners received no allocations under the tax-free route.

As a result, Chinese refiners remain constrained, planning to export just 300 Kt of gasoil this month, with spot export incentives remaining negative throughout December. South Korean refiners will likely need to raise runs to offset the shortfall in Chinese supply.

Residue: HSFO strength remains sticky just as US policy enforcement looms

East of Suez (EoS)

Benchmark Singapore HSFO cracks dipped over the past week, pressured in part by higher regional inventories and changes to China’s fuel oil import duties. Asian HSFO margins could face further pressure from seasonally lower import demand into China during the Lunar New Year holidays beginning in late-January. However, with US President Trump taking office later this month, a stricter sanctions enforcement policy on Iranian fuel oil exports could limit the downside to Asian HSFO cracks. Elevated refinery maintenance in the Middle East will also help keep regional cracks supported until turnarounds gradually start to wind down from February, according to IIR data.

As of January 1, China will raise the import duty on fuel oil by 2 percentage points to 3%, effectively adding $6-$12/t of tax to fuel oil import bills (Argus). This will likely pressure independent refiners’ feedstock demand as the higher costs erode their refining margins which have already faced mounting pressure over the past year from poor domestic demand. In December, fuel oil imports into Shandong dropped to five-month lows of 690 kt, down 48% m/m and 41% y/y, with most of the imports into the region historically originating from Russia, Malaysia, Iran and Venezuela.

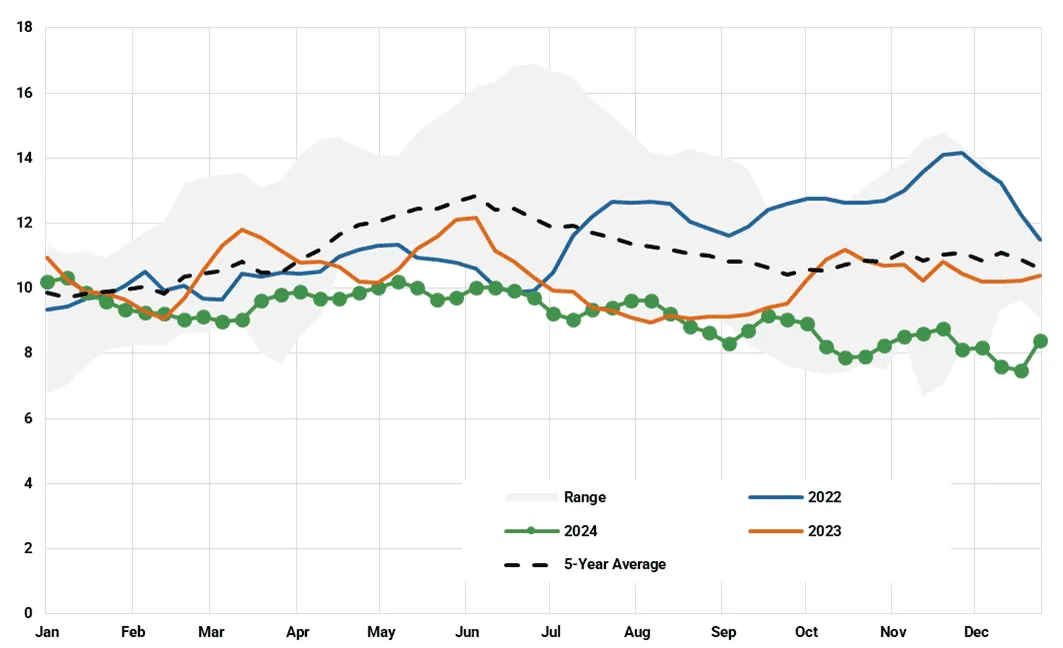

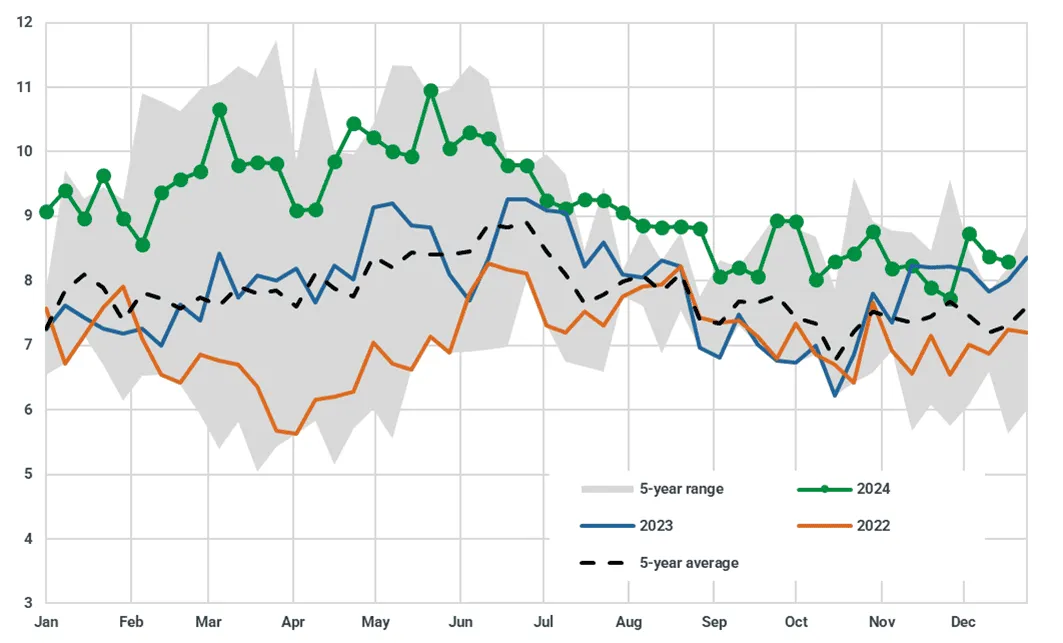

In inventories, Fujairah stocks fell 25% w/w in the final week of December, dragging average 2024 heavy distillate stocks 26% lower from the previous year. Fujairah’s bunkering sales were lackluster for most of 2024 amid stiffer regional competition and limited bunkering demand.

Fujairah: residues inventories level 4-week rolling average (Mbbls)

Source: Fujairah Oil Industry Zone data

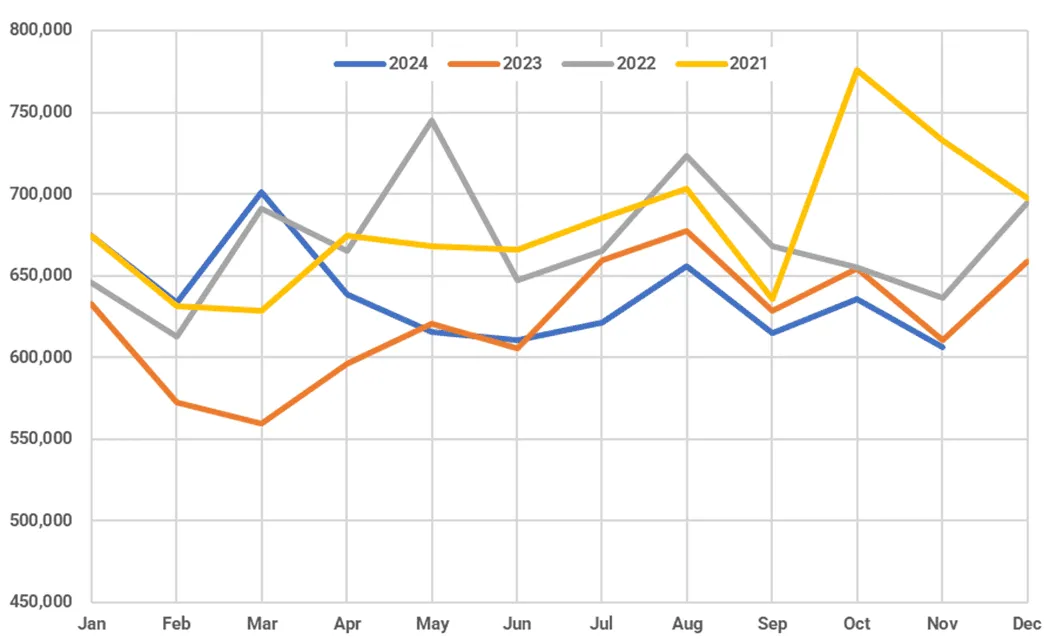

Seasonal Fujairah bunker sales (m3)

Source: Kpler calculations based on Fujairah Oil Industry Zone data

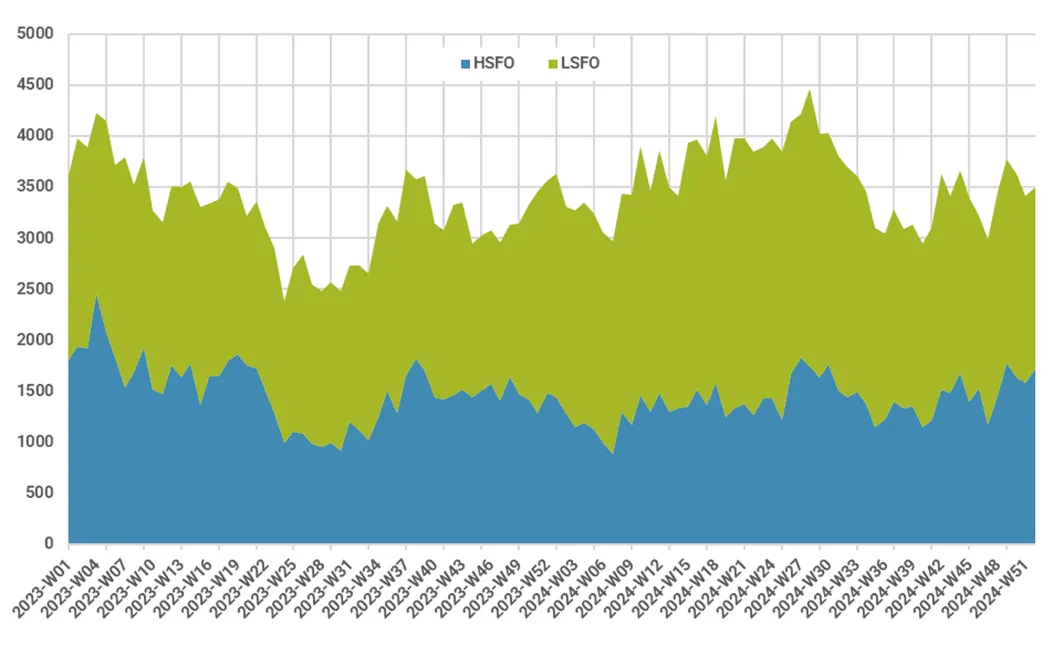

In Singapore, floating storage inventories were mixed with the latest data showing HSFO stocks climbing to a three-week high of 1.72 Kt, while LSFO inventories dropped to a six-week low of 1.78 Kt in the final week of 2024.

Fuel oil FSU inventories around Singapore (kt)

Source: Kpler

West of Suez (WoS)

Like with its counterparts in the EoS, benchmark US and European HSFO cracks dipped over the past week but remain counter-seasonally strong on the back of tight supplies and robust demand.

In the US, the recent weakness in HSFO cracks could extend slightly further amid looming refinery maintenance. Offline primary refining capacity jumps to 1.2 Mbd in January, up from just 120 kbd in December and 150 kbd last year (IIR). US fuel oil imports continue their downward trend, sinking to record lows of 1.71 Mt in December and are projected to slip further to 1.58 Mt in January, helping keep domestic inventories depressed despite a modest recovery in recent weeks (chart below).

In Europe, on the contrary, offline CDU capacity remains steady m/m at 620 kbd in January but is down 24% y/y (IIR), providing pockets of support from feedstocks consumption. EU-27 HSFO/HSSR imports, in the meantime, remain depressed amid ongoing Middle Eastern turnarounds and limited VLSFO arbitrage export opportunities to the east, setting the stage for a pressured VLSFO, and supported HSFO, European outlooks.

ARA: fuel oil stocks in independent storages (Mb)

Source: Kpler calculations based on Insight Global data

US: Weekly fuel oil inventories (Mbbls)

Source: Kpler calculations based on EIA data

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Precise. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get daily expert-driven research through Insight.