ICE gasoil corrects, but upside remains on looming supply tightness

Imports into Europe and the Mediterranean (Med) are set to reach multi-year lows in January and the immediate expectation is for little improvement in extra-regional in the coming months given the state of diesel globally.

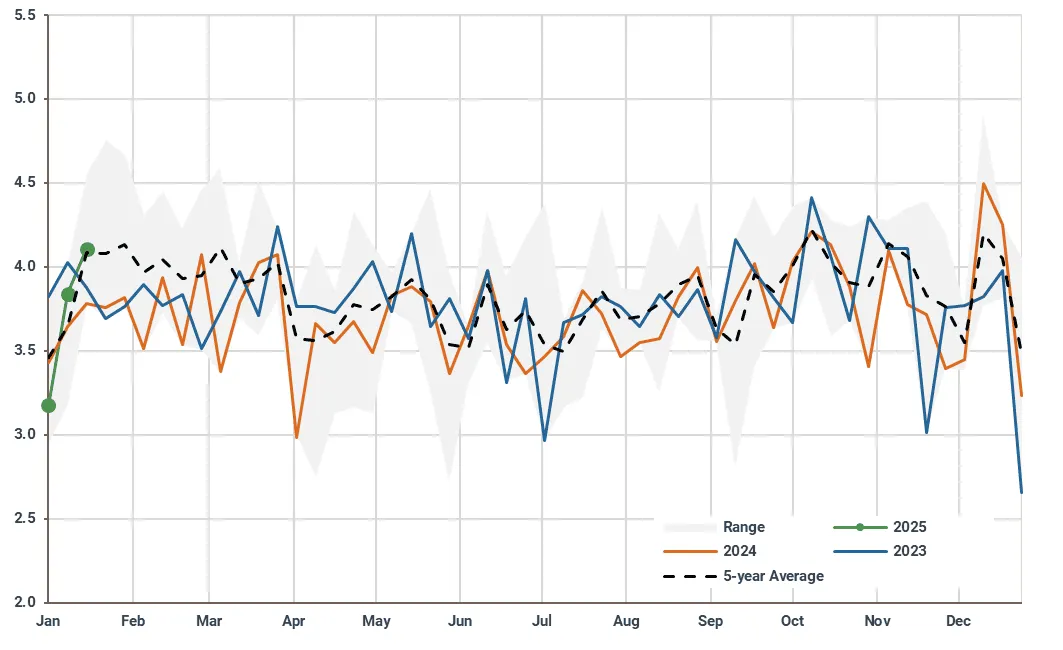

Despite this drop in supply, ICE gasoil spreads are falling (see chart below) due to easing concerns about interruptions to supply from Russia due to recent sanctions. Some readjustment was certainly to be expected but the outlook for the market in Q1 is perhaps stronger than the recent action would suggest. Reduced supply on the horizon and tightening balances overall in Q1 are not having much of an impact currently but we expect this to reverse and be more priced in.

Market and Trading Calls

- ICE gasoil spreads in February to remain strong and likely lift as stocks draw.

- The NWE market in particular should see some upside in light of fewer arrivals and need for supply ahead of spring maintenance.

- It is similar for the Med, but demand so far this year been weak which perhaps lessens the upside.

ICE gasoil spreads ($/t)

Source: Marketview

The drop in flows is partly caused by a closed transatlantic arbitrage – driven by robust heating oil futures sustained by successive cold snaps complicating supply and logistics and seasonal maintenance. We have highlighted in the past our expectations that January would be a strong month for gasoil in the West of Suez driven principally by USGC maintenance and that looks set to continue into February. Demand in the US appears to be robust, shrugging of a weak start to the year (see chart) and diesel inventories remain below the five-year average.

US weekly diesel supplied (mbd)

Source: EIA

It is not just from the US where supply is not forthcoming. A strengthening East-West, a function of European spreads falling after the sanctions shakeout, also means that supply from the region will likely increase a touch but remain diminished. All of which perhaps begs the question why strength has thus far not been maintained in ICE gasoil spreads in order to attract cargoes? In our view, stocks need to be drawn down after the seasonal buildup over December.

So far this has been only modest but we expect this to accelerate as demand increases after January, in a departure of the trend over recent years (see chart below). A Europe that is running down stocks increases the possibility of a stronger market into Q2 once spring maintenance gets underway, in effect deferring strength to later in the year.

To be sure there are signs that there is still weakness in the face of the supply crunch. The Mediterranean market has persistently underperformed its northern counterpart since the start of the year. However, the Med will have upside as shipowners are unlikely to be keen to resume transits via the Red Sea immediately.

ARA gasoil/diesel in independent storages (Mbbls)

Source: Insights Global

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Trade smarter – cut through the noise to find the signal with Kpler's insights