Chinese oil demand continues to underperform

Market bearishness has been driven, at least in part, by struggling Chinese oil demand. In this update, we take a look at the specifics.

Summary

- A largely unimpressive demand environment, namely due to issues in China, has weighed on bullish price impulses. In Q3, we estimate Chinese jet (+26 kbd y/y), gasoline (+80 kbd y/y), and gasoil/diesel (+87 kbd y/y) consumption will struggle to find much growth at all.

- The lack of product demand growth helps explain, at least in part, the dramatic underperformance in Chinese refinery runs. We forecast throughput will finish Q3 at just 15.2 Mbd, marking a decline of roughly 830 kbd against year-earlier levels. Runs will pick up in Q4 to 15.5 Mbd but will remain slightly under levels from the same period a year ago.

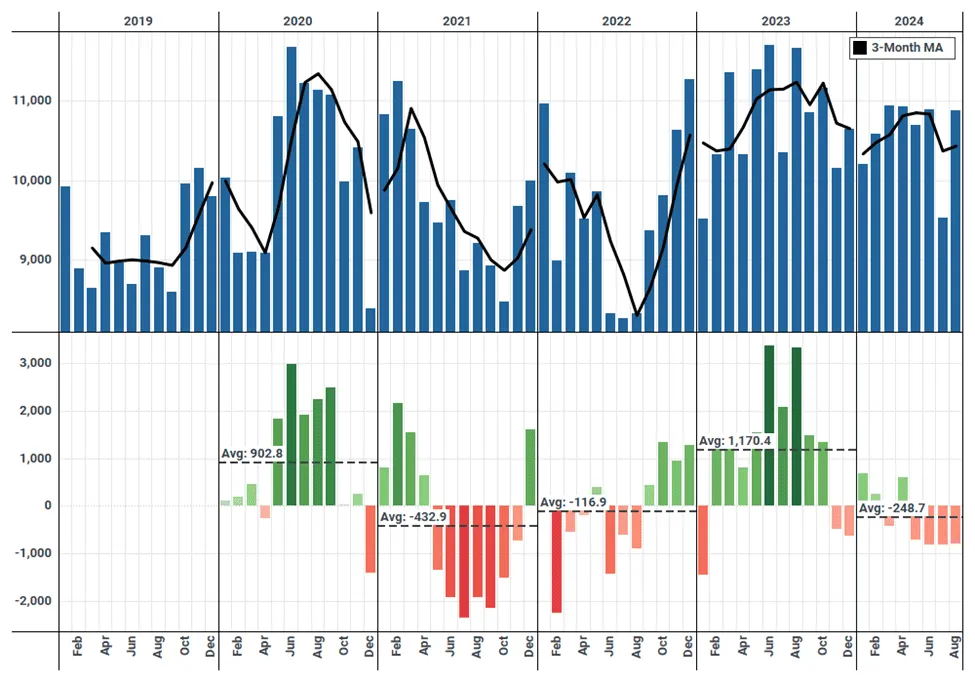

- The impacts of refinery run underperformance are having a material impact on Chinese seaborne crude imports. On a 3-month moving average basis, Chinese oil offtakes are holding at just 10.4 Mbd, down from 10.8 Mbd in June. Arrivals in July (-820 kbd y/y) and month-to-date through August (-800 kbd) are both broadly below year earlier levels.

- Brent speculative positioning certainly appears to be responding to the issues in China. At present, net longs on the Brent contract are holding just above the 52-week low in what has been a second cycle of bearishness that originally took hold in early May.

Despite what is typically the seasonal low point for oil market supply shortages, oil prices have struggled to find much traction in recent weeks. After trading above $85/bbl through June and half of July, Brent spot prices have since traded into a range between $76 and $82/bbl. Part of this is the result of a reevaluation in the geopolitical risk premium. Traders have become increasingly less concerned about an all-out war between Israel and Iran. Oil exports out of Russia have also performed better than expected through July and August. Nonetheless, the issues in Libya, which have effectively removed 1 Mbd from the market, could provide some upward pressure to oil prices in the coming weeks. For a deep dive into these supply-side dynamics, be sure to read our latest update.

We would argue that a largely unimpressive demand environment, namely due to issues in China, have also weighed on bullish price impulses. Chinese product demand is simply not living up to expectations. After a decent start to the year for gasoline and jet demand, in part driven by a robust Lunar New Year travel season, consumption growth has faded. In Q3, we estimate Chinese jet (+26 kbd y/y), gasoline (+80 kbd y/y), and gasoil/diesel (+87 kbd y/y) consumption will fail to find much growth at all with each struggling to post even a 1% gain against year earlier levels.

Monthly Chinese Seaborne Oil Imports (kbd, top) and Y/Y Delta (kbd, bottom)

Source: Kpler; August 2024 data is an average through the first 27 days of the month

The lack of product demand growth helps explain, at least in part, the dramatic underperformance in Chinese refinery runs. We forecast throughput will finish Q3 at just 15.2 Mbd, marking a decline of roughly 830 kbd against year-earlier levels. Seaborne light end and middle distillate exports, particularly through July and August, have also lagged as regional demand conditions have weakened, limiting China’s ability to offload excess supply via the export channel. The export model China has increasingly relied upon across a number of goods and commodities has come under strain this year as countries around the world consider aggressive import tariffs. While we see a pickup in refinery runs through Q4 (15.5 Mbd) as demand seasonally increases for gasoline, and gasoil/diesel, we still do not believe throughput will manage to finish above year earlier levels (15.6 Mbd).

The impacts of refinery run underperformance are having a material impact on Chinese seaborne crude imports. On a 3-month moving average basis, Chinese oil offtakes are holding at just 10.4 Mbd, down from 10.8 Mbd in June. Arrivals in July (-820 kbd y/y) and month-to-date through August (-790 kbd) are both broadly lower against year earlier levels. More broadly, only three out of the first eight months of the year have managed a y/y increase. Chinese onshore oil inventories, after adding roughly 22 Mb to storage between April and July, have since stabilized just above 940 Mb.

Brent speculative positioning certainly appears to be responding to the issues in China. At present, net longs on the Brent contract are holding just above the 52-week low in what has been a second cycle of bearishness that originally took hold in early May. Short positions have surged and continue to hold in a structurally higher region than the period between 2021 and April 2024. Long positions have also been eroded back to the 52-week low, adding further bearish pressure.

Weekly Brent Speculative Positioning

Source: CFTC

China faces a difficult path ahead. After a surge in investment activity through Q1, which required heavy amounts of debt accumulation, industrial production and fixed manufacturing investment growth have begun to flatline or decelerate in Q2 as debt accumulation slowed. China ultimately needs to find a way to rebalance the economy towards household consumption and away from investment. This is a difficult process, made harder by China’s top-down political system. Nonetheless, we have argued for some time that (limited) amounts of additional fiscal stimulus would be made available to households in H2 in an attempt to ensure China’s 5% growth target was met, while simultaneously preventing another Q1 pace of debt accumulation. However, at least for now, such measures remain elusive. Higher consumption growth could help provide support to gasoline and jet demand, and lift refinery runs and Chinese oil use as a result.

Want access to Insights on a regular basis?

Through unbiased, expert-driven research and news, you’ll receive valuable information on supply, demand, and market movements, enabling you to make informed trading and risk management decisions.

Unbiased. Precise. Essential.

Curious? Request access to Kpler Insight today.

See why the most successful traders and shipping experts use Kpler

Get daily expert-driven research through Insight.