October 1, 2024

China’s stimulus' impact on iron ore, steel prices and other commodities

Iron Ore & Steel: China’s stimulus supports iron ore and steel prices

- Global seaborne iron ore exports reached 34.49 Mt in the week beginning 16 September, marking the second-highest volume since July. The increase was primarily due to miners accelerating shipments as the financial quarter draws to a close, particularly those who had curtailed exports in July and August owing to maintenance schedules and subdued demand from China.

- In China, steel output has been continuing to edge higher from the late-August low, with output from China Iron and Steel Association (CISA) members reaching 1.99 Mt/day between 11 and 20 September. However, this remains the fourth-lowest reading so far in 2024 and represents a substantial decline from the 2.13Mt/day during the same period last year. In the short term, we expect output to continue its recovery, particularly as traders intensify their restocking efforts for rebar, with the destocking of old-standard rebar nearing completion. The new rebar quality standards have been in effect since 25 September. However, we continue to expect China’s crude steel output to witness a modest y/y decline across the entirety of 2024.

- In response to the ongoing economic slowdown, Beijing unveiled a fresh round of stimulus measures on 24 September. These include simultaneous cuts to policy rates and the reserve requirement ratio (RRR), which will lower borrowing costs and enable banks to expand lending. For the property market, interest rates on existing mortgages will be cut further, and the minimum down payment on all homes will be reduced to 15%. We believe that these measures would mainly boost market sentiment and stabilise the real estate market rather than increase underlying demand as we believe there is still a long way to go before sentiment among Chinese homebuyers picks up.

- Iron ore and steel prices have been supported by the stimulus announcements. The most actively traded January 2025 iron ore contract on the Dalian Commodity Exchange (DCE) jumped by 6.23% on 24 September and rose by another 1.36% to 709 yuan ($100.82/t) on 25 September (+5.03% w/w), just after closing at the lowest since November 2022 at 658.50 yuan/t ($93.65/t) on the previous trading day. The benchmark rebar and hot rolled coils (HRC) prices at the Shanghai Futures Exchange (SHFE) also surged by 4.21% and 4.20%, respectively, on the same day. At business close on 25 September, these two edged up by 2.38% and 3.44%, respectively, to 3,225 yuan/t ($458.60/t) and 3,306 yuan/t ($470.12/t).

Crude steel output at CISA member mills (Mt)

Source: CISA

Coal: Weekly imports slip despite prolonged summer heat in Asia

- Global seaborne thermal coal trade lost pace last week, falling by around 1.7Mt w/w to 17.83 Mt, as a result of unfavourable weather conditions weighed on deliveries to Chinese ports in the southern part of the country.

- China imported 5.4 Mt of thermal coal last week, down by 1 Mt w/w. This was mainly due to Typhoon Pulasan, which impacted the southern part of the country last week. Thermal coal deliveries to Zhejiang averaged 280,000t/week over 9-23 September, nearly halving from August.

- A prolonged spell of high temperatures was the main driver of Chinese import demand in August, which led to a steep increase of around 25pc in residential power. Temperatures also remained above normal levels in the earlier days of the month, supporting coal generation. But weather conditions started to deviate towards seasonal levels this week, which should reduce the need for coal generation.

- Despite this, Chinese receipts are likely to remain firm, as utilities will look to build stocks after record coal burning this year. Coal stocks at the Bohai Rim fell by around 16pc since July, owing to firm coal burn. Another factor supporting China’s coal import outlook is that imported Indonesian supply still holds a discount against domestic coal.

Guangzhou daily cooling degree days (CDD base 18 °C)

Source: Meteostat

- Coal deliveries to India rose by 400,000t w/w to 3.24 Mt, as high temperatures are driving the increase in power demand in the country. Power demand in northwest India, where most of the imported-coal-fired capacity is located, rebounded sharply since 15 September driving the need for imports.

- Overall receipts in Japan, South Korea edged lower, as power demand boost from the prolonged summer is expected to subside in the coming weeks. Meanwhile, Taiwan’s imports gained by 390,000t w/w.

Germany power generation (GW)

Source: Kpler power

- Elsewhere, in the Atlantic basin shipments to ARA remain below coal consumption levels in the EU, pushing coal inventories lower to the lowest level since March 2022 at 3.43 Mt. Firm wind output reduced the need for coal burn in Germany since the beginning of this month, although coal burn should increase in winter in line with a seasonal decrease in solar generation, which should increase spot demand in the region. Germany coal-fired output averaged 3.2GW, implying a coal burn of around 700,000t.

- Turkish thermal coal imports rose sharply only the week, nearly doubling to 690,000t from last week’s low base. Coal receipts were well below the level required to cover current coal burn levels last week. Turkish coal-fired fleet has been running at nearly full capacity, with output averaging 9.6GW from an installed capacity of 10.4GW over 19-25 September. This is equivalent to around 600,000t/week of thermal coal consumption.

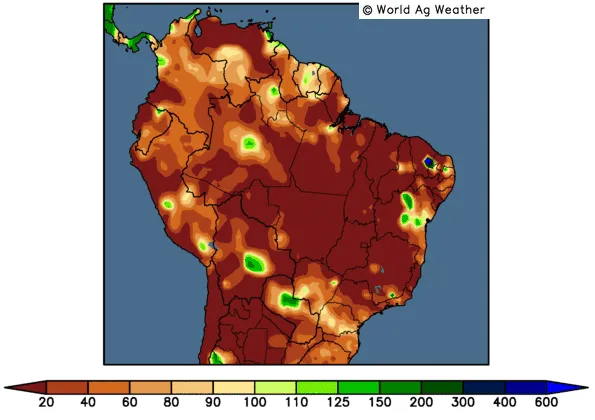

Grains & Oilseeds: Drought in Brazil’s Centre-South threatens soybean planting

- Major soybean producing areas in Brazil, including the state of Mato Grosso continue to see unfavourable planting conditions because of dryness. Soybean planting was allowed since 6 Sep this year and is yet to hit the 1% mark in the state. Futures have rallied about 5% in the last week, with CBOT Mar futures trading at 1093 ¢/bu. It is not too late for rains to improve planting conditions, however, the forecast remains dry. Forecast models differ significantly, with GFS drier than others.

- China is set to receive 7.8 Mt of soybeans in September, an increase of almost 2 Mt y/y and a record for the month. Almost all the oilseeds are coming from Brazil, Uruguay and Argentina. US shipments will only contribute 240 kt. US sales to China have improved in recent weeks as we enter the export season. While China cannot avoid importing from the US, we expect lower total exports to China, resulting in high US ending stocks. South American crop progress and production will affect these assumptions over the next four months.

- Corn exports from Brazil remain weaker y/y. Lower production, weaker demand from China and a continued soybean export program contributed. Q3 exports are expected below 16 Mt, down from 23 Mt last year. Q3 exports to China fell to 1.4 Mt vs. 7.3 Mt last year. Japan, Korea and Vietnam remained major importers.

- Dry weather in Ukraine and Southern Russia is causing concerns over wheat planting in the region. Winter wheat for harvest in July 2025 will be planted now in the region which is suffering from very low soil moisture levels due to lack of precipitation. The forecast remains dry.

30-day past precipitation percentage of normal (%)

Source: World Ag Weather

Minor Bulks: Bauxite and alumina prices rise on supply tightness

- Global seaborne bauxite exports totalled 3.40 Mt last week, in line with the previous 52-week average. Some Australian and Guinean bauxite miners have reportedly raised the prices for the coming fourth quarter as Chinese demand remains strong, despite the coming dry season in Yunnan which may slow hydropower output and thus the pace of aluminium production. This strong demand is largely driven by a continued decline in China’s domestic bauxite output, which has been dropping at a double-digit rate so far this year, following five consecutive years of decline between 2019 and 2023.

- Meanwhile, earlier optimism about Indonesia potentially easing its bauxite export ban has waned as the construction of domestic alumina refineries has made further progress. On 24 September, Indonesia’s President Joko Widodo inaugurated a state-company-owned alumina refinery with a nameplate capacity of 1 Mtpa, which is expected to consume 3.30 Mt of bauxite each year.

- The price of alumina, the intermediate product refined from bauxite, has continued its upward trajectory over the past week following miners’ move to raise bauxite prices. The November 2024 alumina contract on SHFE rose by 2.67% w/w to a near-record high of 4,112 yuan/t ($584.74/t) on 25 September. However, unlike steel and copper, which saw stronger gains following China’s stimulus announcements, aluminium prices experienced much more subdued movement. As of 25 September, the benchmark London and Shanghai aluminium prices only rose slightly by 0.67% and 0.65% w/w, respectively,

Shanghai alumina price again near record high (yuan/t)

Source: Shanghai Futures Exchange

Dry Bulk Freight: China stimulus-driven optimism yet to reach the dry freight market

- At time of writing, Chinese stimulus measures have yet to have any significant impact on dry bulk carrier market sentiment. A modest improvement in Capesize FFAs yesterday was accompanied by a retreat in paper prices for sub-Capesize vessels. The improvement in the larger vessels was consistent with recent movements in the physical market and was not a China-driven sugar rush. Lower bunker prices have weighed on spot voyage rates.

- Reports of increased West Australian iron ore chartering activity have done little to move the dial in the Pacific Capesize market over the past week, with the round-voyage rate only edging slightly higher and the C5 West Australia-China iron ore spot voyage rate almost unchanged. Gains in the Atlantic, where the round-voyage rate climbed by $4,179/day w/w to $22,536/day on 25 September, likely reflected more the required rebalancing of earnings between the two basins to draw in ballasting tonnage, than any upsurge in North Atlantic chartering demand. The Atlantic round-voyage rate had been at a discount of more than $11,000/day to the Pacific equivalent, this has now reduced to around $8,000/day, and scope remains for a further rebalancing. This left the Capesize TC average slightly higher w/w at $27,495/day on 25 September.

- Sub-Capesize markets saw modest gains overall across the past week. The increases were on Pacific coal routes from Indonesia into China and India. The BSI (63.5 kdwt) S8 route (South China-East Coast India via Indonesia) rose by $2,111/day w/w to $18,207/day on 25 September. Vessel supply in the region has been tightened by the short-term planned closure of some ports in North China due to military exercises in the Bohai Bay region. Demand has also been supported by warm weather-driven demand in China and India.

Atlantic Capesize earnings continue to lag the Pacific ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Want access to Insights on a regular basis?

Through unbiased, expert-driven research and news, you’ll receive valuable information on supply, demand, and market movements, enabling you to make informed trading and risk management decisions.

Unbiased. Precise. Essential.

Curious? Request access to Kpler Insight today.

See why the most successful traders and shipping experts use Kpler

Request a demo

Get daily expert-driven research through Insight.

Request access

.png)