Asian LNG and TTF prices to hold steady after Ukraine’s acceptance of a temporary ceasefire sees limited market impact

Market & Trading Calls

European TTF price outlook: Stable as temperatures and renewable energy output are forecast to increase gradually in the coming days. This will be balanced by a slight decrease in net pipeline gas flows into the EU and the need to maintain NW Europe netbacks at a premium to keep attracting LNG supply.

Asian LNG price outlook: Stable, buoyed by steady European TTF price expectations, mild weather forecasts for Northeast Asia, and ample Pacific supply—balancing out upward pressures from restocking in South Korea and growing demand in South and Southeast Asia.

TTF-Asian LNG spread: Stable as both TTF and Asian LNG prices are projected to follow a steady trend. As of 12 March, Asian LNG prices hold a $0.20/MMBtu premium over the European TTF, with the spread narrowing by $0.52/MMBtu since last week due to TTF rising and Asian LNG declining slightly.

US Henry Hub price outlook: Bearish as above-average temperatures are forecast for nearly all of the Lower 48. Despite the geopolitical risks playing havoc with prices in recent weeks, weather conditions seemingly stepped into the forefront this week.

Key natural gas and LNG prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF spread ($/MMBtu)

Source: ICE, Kpler Insight

TTF prices to hold steady after Ukraine’s ceasefire agreement triggers limited market reaction

European TTF front-month prices rose last week, closing at $13.48/MMBtu on 12 March, up $0.47/MMBtu (+3.6%) from 5 March. Prices climbed steadily from 6–11 March as weather forecasts revised temperatures lower for 12–18 March, while weaker-than-expected wind output in NW Europe provided additional support. Further price strength likely stemmed from Europe’s need to maintain LNG netbacks at a premium to Asia to secure supply. On Wednesday, 13 March, the news about Ukraine’s acceptance of a 30-day ceasefire with Russia had little impact on European gas prices as, in our view, it is unlikely that this will restore the transit of Russian gas via Ukraine in the short term.

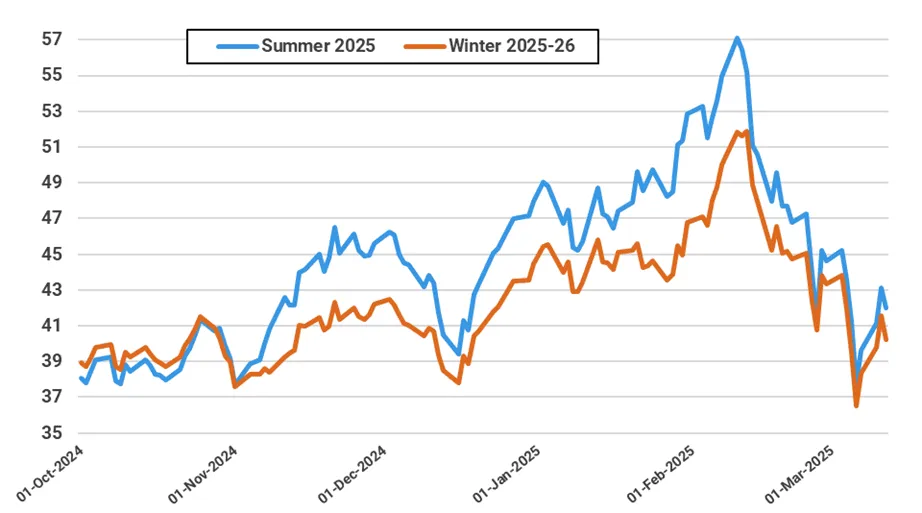

The seasonal (winter 2025-26 - summer 2025) price spread closed at -$0.44/MMBtu, slightly widening by -0.02 from last week. However, it is still far from the -$1.83/MMBtu mark reached earlier towards the end of January.

TTF summer and winter prices (€/MWh)

Source: Argus

Kpler Insight anticipates TTF front-month prices remaining range-bound next week. Temperatures and renewable energy output are forecast to increase gradually in the coming days. However, this will be balanced by a slight decrease in net pipeline gas supply into the EU and the need to have NW Europe netbacks at a premium to Asia to keep attracting most LNG exports from Western Africa.

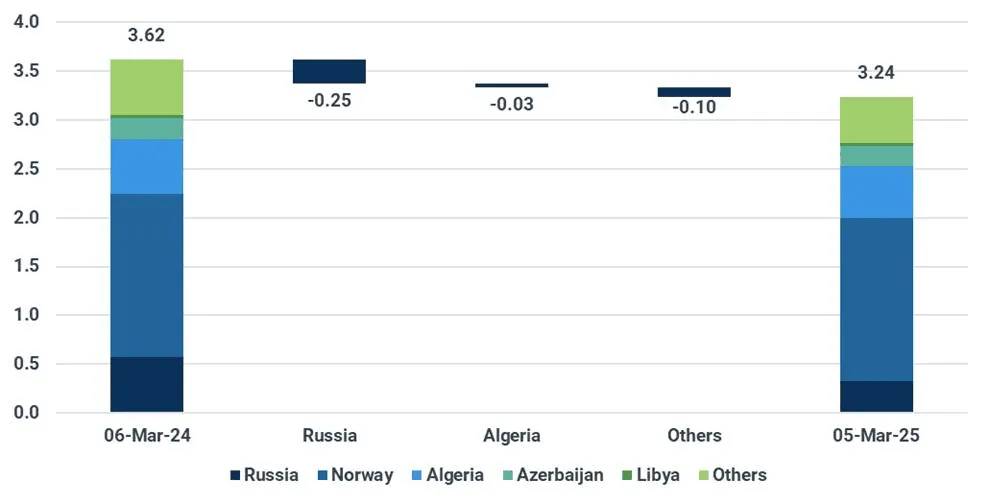

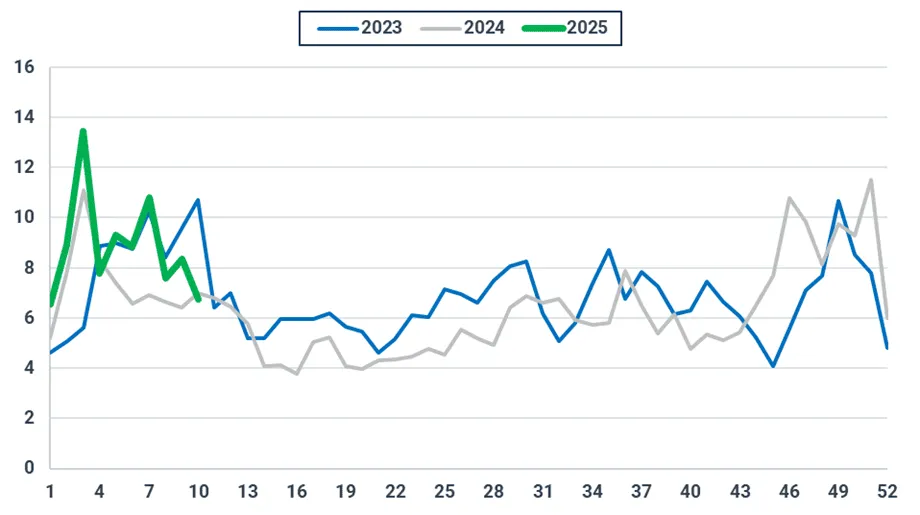

Expanding on fundamentals, Norwegian gas flows to France remained robust, with arrivals at Dunkerque staying above the 40 Msm3/d mark since early March, while those to St Fergus (UK) remained low. However, Turkstream flows to the EU have dropped significantly in the past few days, correlating well with lower flows from Bulgaria to Serbia, likely due to lower regional consumption. Conversely, Libyan flows increased to 0.028 bcm for the week starting 15 March (2.8x higher w/w), while overall Algerian exports gradually recovered from a temporary reduction observed between 8-10 March.

EU-27 weekly net pipeline gas imports (bcm)

Source: Kpler Insight. Data represents week commencing 19 and 26 February 2025.

EU-27 weekly net pipeline gas imports (bcm), y/y comparison

Source: Kpler Insight

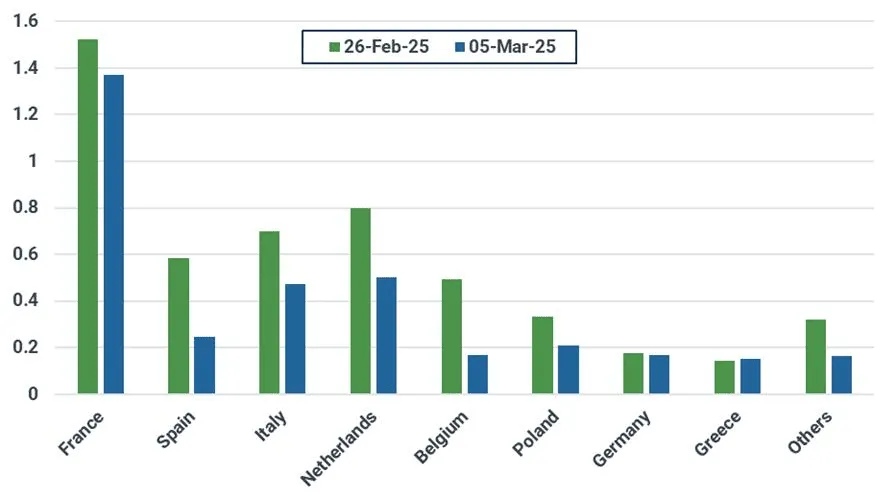

EU-27 LNG imports dropped to 3.4 mcm last week (-32% w/w), with decreases across all major buyers, particularly Spain. Lower LNG imports to Spain were likely the result of LNG cargoes going to destinations with higher prices, such as Turkey and the UK, whose weekly LNG imports remain strong.

EU-27 weekly LNG imports (mcm)

Source: Kpler Insight. Data represents week commencing 19 and 26 February 2025.

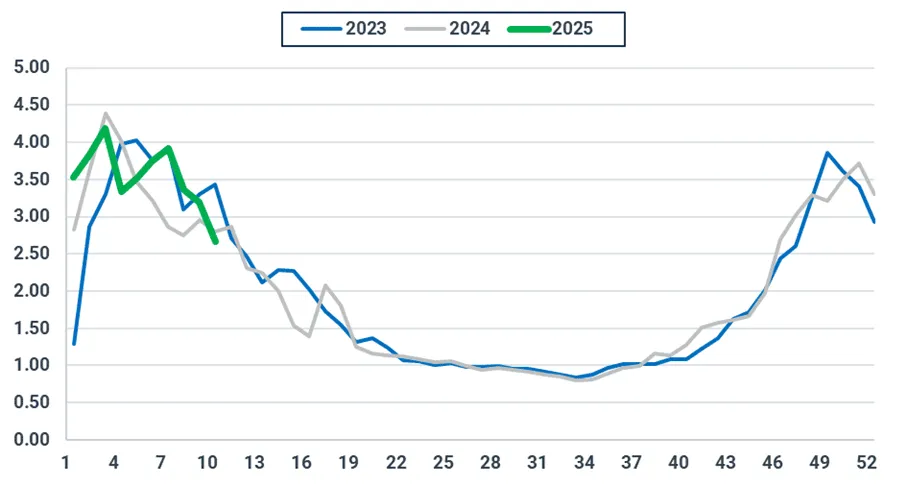

On the demand side, weekly gas consumption from local distribution in 15 EU countries is estimated to have fallen by 16.7% w/w to 2.66 bcm, marking a third consecutive week of losses. This is the lowest level recorded since around mid-November last year. The decline was driven by above-average temperatures across Europe, with weekly losses nearing 30% in the Netherlands, Belgium, and Austria.

Looking ahead, forecasts indicate that temperatures will drop to approximately 3°C below average across Northern Europe until March 19–20, likely increasing gas demand for heating. Beyond that, temperatures are expected to rise above seasonal norms.

EU-15 weekly consumption in the local distribution (res/com) sector (bcm)

Source: ENTSOG, ENAGAS, Eurstream, AGCM, Kpler Insight. The EU-15 perimeter includes AT, BE, CZE, FR, HU, GRE, ITA, NL, LUX, POL, POR, ROM, SLVN, SLVK, and SPA.

Average forecast temperatures for selected European countries (°C)

Source: Kpler Power. As of 13 March 00:00 UTC.

On the power side, EU-27 gas-fired generation fell by ~19% w/w to an estimated 6.74 TWh, as rising solar output and lower overall power demand outweighed the impact of slightly weaker wind generation.

Looking ahead, gas-fired generation is expected to rise next week with the return of colder temperatures in Europe. However, improving wind output and stronger solar generation should help cap consumption gains.

EU-27 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight

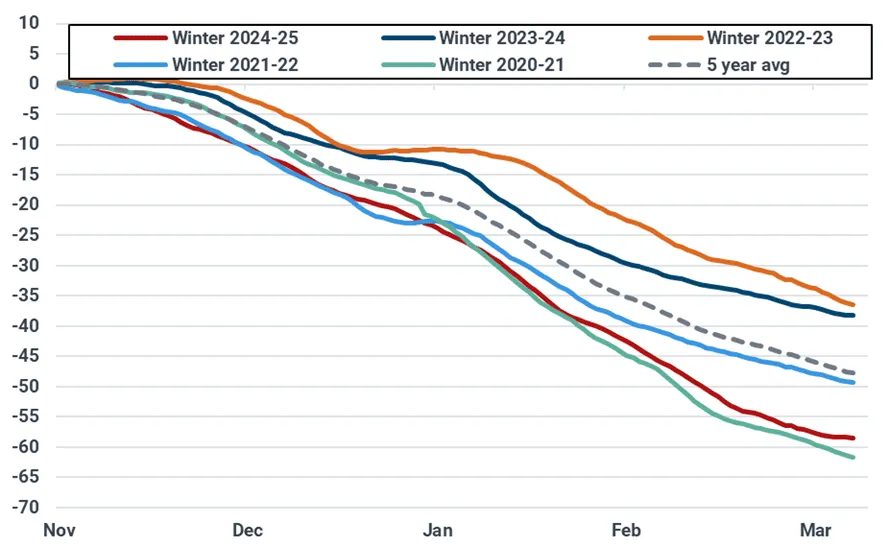

As of 11 March, EU-27 underground storage levels stood at 36.2% full. The pace of withdrawals slowed down in NW Europe due to warmer temperatures and higher Norwegian flows to the EU. It was noted that Slovak and Polish gas exports to Ukraine were close to null, highlighting lower Ukrainian demand and thus reducing the pace of storage withdrawals in the wider CEE region despite Hungarian exports to Ukraine remaining stable.

Lower temperatures for the next 7 days may accelerate the pace of withdrawal rates next week.

EU-27 daily underground storage net withdrawals since 1 November (bcm)

Source: GIE, Kpler Insight. Latest date as of 11/03/25.

Want the complete report?

The full report is available within Insight and contains:

- Asia: Prices steady amid mild weather, ample supply, expectations of Northeast Asian restocking, and rising price-sensitive demand

- US: Henry Hub prices to drop below $4/MMBtu as warm weather blankets the Lower 48

- LNG Supply: Strong global exports persist amid robust US exports and Nigerian recovery; LNG Canada cooldown cargo set to arrive 1 April

- Key indicators

Stay ahead of the curve with up-to-the-minute news and forward-looking views on market-moving developments covering LNG, European natural gas and US natural gas markets. Get daily LNG reports and understand the interplay between natural gas, LNG, and coal including supply and demand fundamentals.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data